Open Enrollment: Active vs. Passive Benefits Election

There are advantages to active enrollment, but first understand what the process entails

This is the first in a series of articles on meeting open enrollment challenges. This article examines the pros and cons of requiring employees to proactively elect to enroll in health and other benefit plans for the coming year (active enrollment) versus allowing their current benefit selections to automatically roll over unless they elect to change them (passive enrollment).

The consensus view among employee benefit advisors is that active open enrollment is the superior way to prod employees to make appropriate decisions about the benefits that will best suit their own—and their families'—needs. Active enrollment, however, requires that HR benefit managers engage directly with employees to ensure that no one inadvertently misses their opportunity to elect coverage for the new year.

If employees fail to make their selections before the end of the open enrollment period, they'll have to wait until the following year's open enrollment to sign up for benefits—unless they experience a qualifying life event such as getting married or divorced, having a baby, or a spouse losing his or her job. The possibility of inattentive employees being left without health and other benefits—and the outcry from those who might find themselves in this predicament—keeps most employers on the passive enrollment track.

A 2011 study found that 71 percent of U.S. employers opted for passive enrollment.

"The fear is that if your employees don't sign up, they'll lose their coverage," said Kim Buckey, vice president of compliance communications at Birmingham, Ala.-based DirectPath, an employee engagement and health care compliance firm. To make certain that doesn't happen, she said, HR professionals should launch an effective communications campaign and offer one-on-one personal support throughout the enrollment process to ensure that no employee gets left behind.

Active Enrollment Advantages and Concerns

"Employers that require participants to annually examine their benefit elections are better able to drive employees to more cost-effective coverage, such as a high-deductible health plan," when appropriate, Buckey noted. "They can build employee loyalty by highlighting the competitiveness of their benefits package. In addition, they can capture critical beneficiary and dependent information for dependent audits"—ensuring that health care dollars are spent only on those who are entitled to coverage.

Employers also are more likely to retain employees who understand the relative value of their benefits package. Active enrollment helps ensure that they do.

When provided with the opportunity to revisit their benefit choices—and when given benefit guides, interactive tools and access to one-on-one decision-making support—"employees can ensure that their benefit coverage matches their current family situation and needs," Buckey said. "They're more likely to learn about and understand how those benefits work, and they have a better appreciation of what their choices during the year will cost them out of pocket."

"There are obviously advantages of having an active enrollment from an engagement standpoint," said Taylor Clausen, director of key accounts at Jellyvision, an employee communication software provider based in Chicago. "It accentuates employees' attention" to changes being made to benefit offerings. However, "from the employer's standpoint, to pull off an active enrollment can be a large undertaking for everyone involved, not only the employer but their various vendor partners that are going to be involved in executing employee elections. It amplifies the effort for everybody."

"People take things for granted or aren't always in tune with the effect that a life-status change could have, or might not be aware of new benefits their employer might be offering," said Meredith Ryan-Reid, senior vice president at benefit provider MetLife's group benefits division in New York City. "There's always a need to update information, even things as simple as noting an address change or adding a beneficiary."

When employees don't update their records annually, it can leave employers and insurance carriers "struggling just to make sure they have all the relevant information" for employees, she said. Active enrollment makes it far more likely records will be kept up to date "because employees actually have to go in and make a decision."

With active enrollment, MetLife found, employees were three to five times more likely to participate in available voluntary benefit plans, Ryan-Reid pointed out. Voluntary benefits can range from supplemental critical illness coverage to pet insurance, and typically have group-rate premiums negotiated by the employer but paid by employees, sometimes on a pretax basis through salary-deferral contributions.

Active enrollment also "prompts employees to opt out of certain coverages they might discover they don't need anymore," such as supplemental life insurance if their children are now grown and self-supporting, Ryan-Reid noted.

"If you're not requiring people to go in and make a choice every year, you just can't grab people's attention," she said. "It's one of those tough-love approaches where you want to make sure that people take the time to make good decisions for their own best interest."

[SHRM members-only toolkit: Designing and Managing Flexible Benefits (Cafeteria) Plans]

Confronting Employee Inertia

As to the possibility that employees won't respond and will lose their benefits, "that's always been the fear, and it requires communication and outreach to employees," said Ryan-Reid. As the end of the enrollment window approaches, those who haven't made an election should be contacted to verify that it is their intent not to participate (for instance, if they have health coverage through a spouse's plan).

If employees receive reminders leading into open enrollment and then at least weekly throughout the enrollment period, through a variety of media channels—e-mail, postcards, benefit brochures and posters displayed in the workplace, for instance, in addition to required annual benefit disclosures—"it's pretty hard for them not to pay attention," she noted. "Companies have so many ways to reach employees now, including social media platforms, that we haven't heard too many horror stories" of employees stranded without health coverage.

As a last resort, if employees haven't enrolled, haven't indicated that their failure to participate was intentional and are not responding to HR's requests, consider contacting the employee's manager and ask that that he or she ensure that the employee understands that failure to elect coverage means no employer-sponsored benefits next year.

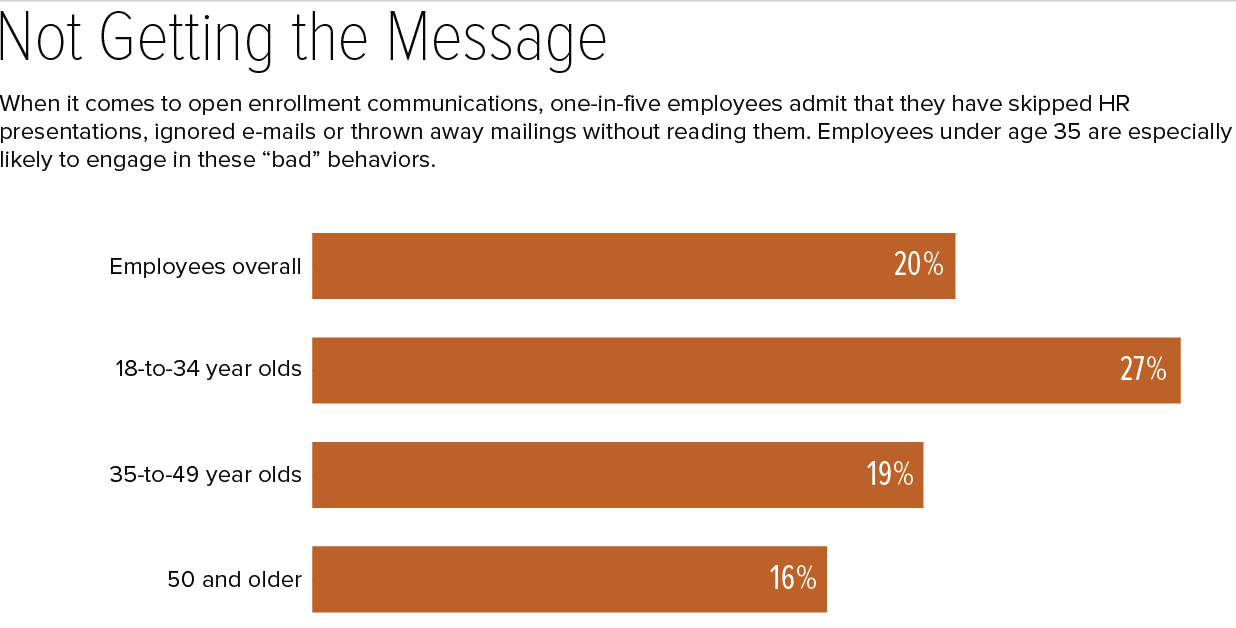

Source: Jellyvision's 2017 ALEX Benefits Communications Survey, conducted in February and March 2017, based on responses from 2,043 U.S. adults employed full-time and eligible for company provided benefits. |

Making the Shift

"When shifting to active enrollment, make sure people know that things are different this year," said Kirk McConnell, product marketing lead at Collective Health, a health benefits administration firm in San Francisco. "Don't be afraid to be a little jarring," he added. Be direct and hammer the point home, such as sending an e-mail with the subject line "No Election = No Benefits."

While benefit specialists make a strong case for active enrollment, a middle path may be to use this approach only when making significant changes to benefit offerings.

"When there is a plan design change that is relatively significant, employers might want to consider active enrollment for the upcoming year," said Jellyvision's Clausen.

"From a trend standpoint, we saw quite a bit of that last year, as employers pulled various plan design levers to try to curb costs and to better serve their employees" by altering health plan options, Clausen noted. Employers could then revert back to passive enrollment for years without significant plan design changes.

This is the first in a five-part series of articles on meeting open enrollment challenges. The second installment is Open Enrollment: Developing Your Game Plan.

Also in this series:

Part Three: Open Enrollment: Targeted Communications Address Differing Needs

Part Four: Open Enrollment: Using Social Media and Decision-Support Tools

Related SHRM Resources:

Open Enrollment Guide & Resources Page

Was this article useful? SHRM offers thousands of tools, templates and other exclusive member benefits, including compliance updates, sample policies, HR expert advice, education discounts, a growing online member community and much more. Join/Renew Now and let SHRM help you work smarter.

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.