For Employees Approaching Retirement, Health Coverage Decisions Loom

Part 4: Medicare rules and costs are a mystery to many, but don't overlook HSAs

PART 1

Easing into Retirement

Targeted Benefits for Aging Workers

PART 3

Lifetime Income Prospects

Part 4

Preparing for Health Care in Retirement

Older workers face a number of decisions about health care coverage, such as whether to enroll in Medicare while still employed and if so, which parts. They should also plan for the coverage they'll need in retirement, both immediately after leaving work with COBRA as an option if they're not yet Medicare-eligible, and long-term to fill Medicare's gaps. And they should understand the role health savings accounts can—and can't—play.

Among Baby Boomers, "the biggest stress trigger around retirement is their ability to afford health care," said Meghan Murphy, vice president of thought leadership at Fidelity Investments, a benefits administrator, in Boston. A 65-year-old couple retiring in 2019 can expect to spend $285,000 in health care and medical expenses throughout retirement, she noted, while for single retirees, the health care cost estimate is $150,000 for women and $135,000 for men, based on Fidelity's research.

Below are key health coverage issues that confront aging workers and the options they'll face.

Medicare Basics

As reported earlier this year by SHRM Online, as employees become eligible to enroll in Medicare at age 65, there are several parts to Medicare with varying premiums that employees should keep in mind:

Part A covers hospital and other inpatient care, and most enrollees are not charged a monthly premium. Many employees who continue working will enroll in Part A unless they want to continue contributing to a health savings account (HSA), which is incompatible with any part of Medicare.

Part B covers doctor visits and outpatient exams and tests and charges a monthly premium.

Part C refers to Medicare Advantage plans sold by insurers. These plans charge monthly premiums and provide coverage compatible with Medicare but with different out-of-pocket costs and rules.

Part D covers prescription drug costs. These privately administered plans charge a monthly premium.

Employees may choose to wait until they stop working to enroll in Medicare. However, if they do so, they must be able to provide proof they had employer-sponsored coverage (or coverage through their spouse's employer), including prescription drug coverage at least equivalent to Medicare Part D's, or they will face higher Medicare premiums if they delay Medicare enrollment.

Enroll in Medicare or Not?

"From the employees' perspective, the question is whether they are better off with Medicare or their employer's plan, and that decision requires a facts-and-circumstances analysis," said Liliana Salazar, chief compliance officer for western region employee benefits at health insurance brokerage HUB International in Los Angeles.

When deciding which plan to choose, she advised, employees should consider what their employer plan covers, whether the plan is generous enough to cover the majority of their out-of-pocket expenses and if the plan exposes them to large out-of-pocket expenses.

Medicare premiums are usually deducted from Social Security benefits. However, if employees delay receiving Social Security payments after age 65 but still enroll in Medicare Part B, they would pay Part B premiums—and potentially Part D premiums—on an after-tax basis while receiving employer-sponsored coverage, she noted.

"The reality is that most employees turning 65 will stay enrolled in their employer's group health plan," Salazar said. "It's a known program, it's easily accessible, and Medicare is very complicated." Also, she explained, "Medicare secondary-payer rules prohibit employers from creating any incentives, monetary or otherwise, to encourage individuals to transition away from the employer-sponsored plan."

Older workers, however, may be too hasty in deciding not to shift to Medicare as a replacement for their employer's plan, said Tricia Blazier, director of health care insurance services at Allsup in Belleville, Ill. She gave these reasons why Medicare plans might be a better option for some employees:

- Medicare premiums are relatively stable. For example, the standard Part B premium is currently $135.50, up only slightly from $134 in 2018, which was unchanged from 2017. Private insurance plan premiums, in contrast, have far outpaced inflation over the past decade.

- Medicare has low deductibles—under $200 for most plans.

- With employer plans, 66 percent of workers have a co-pay. With Medicare, out-of-pocket costs are lower and may be eliminated.

- Medicare has significant cost savings if employees primarily use generic prescription medications, so it can pay to take a look at Part D plan options.

- Medicare allows enrollees to personalize their health care coverage so they can ensure it addresses their needs, including in-network doctors, whereas "employers may provide a one-size-fits-all plan for their workforce," Blazier said.

While choosing Medicare over an employer's plan "may not be the right choice for everyone, it's certainly an option," she added.

State health insurance assistance programs, available in all 50 states, offer free Medicare enrollment counseling and assistance.

Medicare Prescription Drug Coverage

Plan sponsors that offer prescription drug coverage must provide notices of creditable or noncreditable coverage to those who are Medicare-eligible before each year's Medicare Part D annual enrollment period. Prescription drug coverage is creditable when it is at least equivalent in value to Medicare's standard Part D coverage and noncreditable when it does not provide, on average, as much coverage as Medicare's standard Part D plan.

The obligation to provide these notices is not limited to retirees and their dependents, but includes Medicare-eligible active employees and their dependents and Medicare-eligible COBRA participants and their dependents. The Centers for Medicare & Medicaid Services provides a Creditable Coverage Simplified Determination method that plan sponsors can use to determine if a plan provides creditable coverage.

"Disclosure of whether their prescription drug coverage is creditable allows individuals to make informed decisions about whether to remain in their current prescription drug plan or enroll in Medicare Part D during the Part D annual enrollment period," noted Richard Stover and Wai Kin Chan, consultants with HR advisory firm Buck.

COBRA or ACA Exchange?

If retiring before age 65, employees should consider whether to elect COBRA or to buy coverage from the Affordable Care Act's (ACA's) online exchange, Salazar said. Employees should ask, "Will I qualify for a subsidy under an exchange-purchased plan, and would that be more cost-effective than enrolling in my employer's COBRA plan?"

[SHRM members-only toolkit: Employing Older Workers]

Addressing HSA Confusion

Jeanne Thompson, head of workplace solutions thought leadership at Fidelity, explained that often, "those who are about to retire are just realizing that Medicare isn't free. Many employees have money in their HSA but don't understand how these accounts actually work once they retire."

Since Medicare, as noted, is incompatible with making new HSA contributions, employers should help employees understand why, if they're age 65 or older, they should do the following:

- Stop making contributions to their HSAs six months before they enroll in Medicare, or risk tax penalties. Once individuals enroll in Medicare, this coverage is retroactive up to six months before they signed up (but not beyond their initial month of eligibility, which is generally the month of their 65th birthday).

- Not delay signing up for Medicare for more than seven months after retiring. This means not opting to take COBRA coverage beyond the seven-month post-employment window for enrolling in Medicare, or they'll face significantly higher Medicare premiums throughout their lifetime.

But while Medicare-enrolled retirees are no longer eligible to contribute to their HSA, they still can use the account's funds to pay premiums for Medicare and long-term care plans, as well as for out-of-pocket health care expenses.

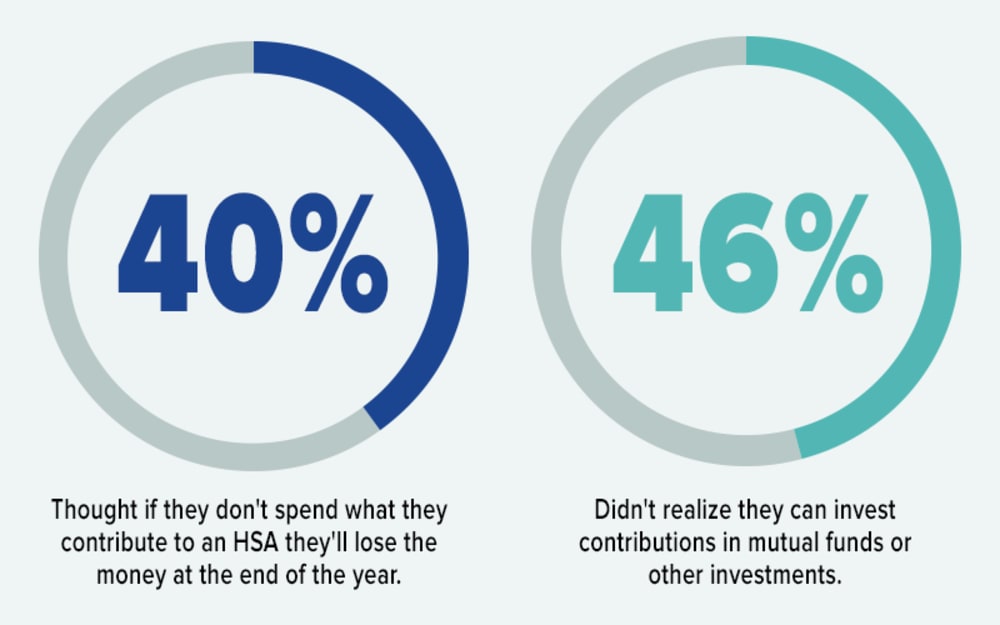

HSAs are a potential retiree health care account, Thompson said, but "many don't realize their HSA dollars are not 'use it or lose it' at the end of the year like a flexible spending account. Or they don't understand the triple tax advantages of contributing, growing and withdrawing funds tax-free" when used for health care. In comparison, withdrawals from a traditional 401(k) plan are taxed as income, and Roth 401(k) contributions are made with after-tax dollars.

Significantly, "many don't realize they can invest HSA funds within the account in mutual funds, as they do with their 401(k) plan, for long-term account growth," Thompson noted.

HSA Misconceptions Impede Saving for Retirement Health Care

While more employees are contributing to a health savings account (HSA), a recent survey of 1,309 HSA account holders found misconceptions that could lead many to fail to maximize this benefit for long-term health care savings, including in retirement.

Among the more than 800,000 HSAs managed by Fidelity Investments, only 7.7 percent of account owners invested any portion of their savings last year.

Source: Fidelity Investments.

Only about 8 percent of people who have an HSA are actually investing the money, Murphy pointed out, although "we're seeing a shift toward using HSAs, at least in part, for retiree health care."

Not everyone can afford to accumulate funds in their HSA for long-term investment and growth, she acknowledged, "but for those that can, it's an amazing opportunity to save besides your 401(k)" for health care during retirement.

Related SHRM Articles: Employees Still Perplexed by HSA Plans During Open Enrollment, SHRM Online, October 2019 Medicare-Eligible Employees Pose HR Challenges, SHRM Online, February 2019 Early Retirement Health Care Quandary Keeps Workers on the Job, SHRM Online, July 2017 |

Related Articles

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.