Reporting CEO-to-Employee Pay Ratios: Navigating the Minefield

Making sense of the Frank-Dodd Act's pay disclosure requirement

Update: On Aug. 5, 2015, the Securities and Exchange Commission issued a final rule requiring publicly traded companies based in the U.S. to disclose how median employee pay compares with CEO compensation, known as the CEO pay ratio. See the SHRM Online articles SEC Pay-Ratio Rule Spotlights CEO Compensation and Determining CEO Pay Ratio Isn’t So Simple. |

The Dodd-Frank financial reform legislation enacted in July 2010 includes a pay disclosure rule that will require many U.S. companies to report the ratio of CEO pay to median employee pay in annual proxy statements. The requirement has sparked lively debates and questions concerning the utility of this ratio, how it is calculated and the potential for it to be misleading and misused.

Section 953(b) of the Dodd-Frank Wall Street Reform and Consumer Protection Act will require all U.S. public companies and companies that are not publicly traded but have public debt, as well as other companies that are required to file reports with the U.S. Securities and Exchange Commission (SEC), to disclose the following compensation metrics:

1. The annual total compensation of the chief executive officer. The annual total compensation for the CEO is currently available in the summary compensation table in SEC Form DEF 14A Filings (i.e., definitive proxy statements).

2. The median annual total compensation for all employees (except the chief executive officer).

3. A ratio of these two metrics:

Annual Total Compensation of the CEO |

The median annual total compensation metric for all other employees (#2 above) and the CEO-to-employee pay disparity ratio (#3) are new requirements.

On the surface, these metrics might seem relatively simple and reasonable to calculate. However, digging into the data—and considering the complexity of factors that influence the numbers—reveals that the CEO-to-employee pay ratio defined by the Dodd-Frank Act can be difficult to calculate and interpret.

We thought it would be instructive to take a closer look at this new pay disclosure requirement and calculate CEO-to-employee pay ratios from the Culpepper Compensation Survey database. The analysis includes data collected from public and private technology and life science organizations reporting prior-year compensation data for full-time employees in the United States. Statistics for part-time employees and employees located outside of the United States were excluded.

Defining Total Compensation

Before diving into the numbers, it is essential to define total compensation and understand the elements of compensation included in the calculations.

The SEC defines total compensation in Item 402 of Regulation S-K. Annual total compensation includes the sum of salary, bonus, stock awards, option awards, non-equity incentive plan compensation, change in pension value and nonqualified deferred compensation earnings, and all other compensation (e.g., perquisites, personal benefits and property with an aggregate amount exceeding $10,000; tax gross-ups; company contributions to defined contribution retirement plans; preferential stock purchase discounts; preferential life insurance premiums; and dividends or other earnings not factored into the fair value of equity awards).

The SEC's definition and calculation of total compensation includes the value of some but not all company provided benefits. For example, it includes retirement benefits, such as company contributions to 401(k) and other defined contribution plans, and changes in pension values. However, it does not include the value of other benefits available on a nondiscriminatory basis to all employees. That would exclude company contributions to group insurance plans (e.g., health, life and disability insurance benefits) and to health savings accounts.

The pay disclosure requirements in the Dodd-Frank Act will require many companies to start calculating total compensation for every employee so they will be able to calculate the CEO-to-employee pay ratio.

Because of the administrative burden of reporting the value of perks and benefits provided to individual employees, this analysis did not require survey participants to provide this level of data for each employee. For purposes of the analysis, CEO-to-employee pay ratios were not calculated using the SEC's definition of total compensation. Instead, CEO-to-employee pay ratios were calculated for three commonly used compensation metrics:

• Annual base salary—guaranteed, short-term, non-variable cash compensation.

• Annual total cash compensation—the sum of base salary plus cash allowances plus bonuses plus commissions plus cash profit sharing plus other forms of variable cash payments.

• Annual total direct compensation—the sum of total cash compensation plus total fair value of all annual long-term incentives (e.g., stock option awards, restricted stock shares/units, performance stock shares/units, phantom stock shares, stock appreciation rights and long-term cash awards).

U.S. CEO-to-Employee Pay Ratios

In the U.S., the median value of the ratio of CEO total direct compensation to the median total direct compensation of all other employees is 5.4. In other words, the typical CEO's total direct compensation is approximately five to six times larger than the median total direct compensation of all other employees in their organization.

However, to put this ratio into context, it is important to consider a variety of factors, particularly company size (e.g., annual revenue, number of employees, market capitalization). As companies increase in size, the multiple of CEO compensation to employee compensation increases. This is consistent with the principle that company size is typically the predominant factor influencing executive compensation.

CEO-to-Employee Pay Ratios by Annual Revenue | |

| Median value of Ratio of CEO Pay to Median Pay of All Other Employees |

Annual | Annual | Total Direct Compensation | |

All U.S. companies | 4.0 | 5.6 | 5.4 |

Annual revenue (millions) |

|

| |

Up to $5M | 2.3 | 2.3 | 2.3 |

Over $5M to $10M | 2.4 | 2.7 | 2.7 |

Over $10M to $50M | 3.0 | 3.5 | 3.5 |

Over $50M to $100M | 4.0 | 5.2 | 5.2 |

Over $100M to $250M | 4.6 | 6.9 | 7.3 |

Over $250M to $1,000M | 6.7 | 10.4 | 12.5 |

Over $1,000M to $2,500M | 10.7 | 21.8 | 33.2 |

Over $2,500M | 16.0 | 36.5 | 91.6 |

Source:Culpepper Compensation Surveys U.S. Database, October 2010 |

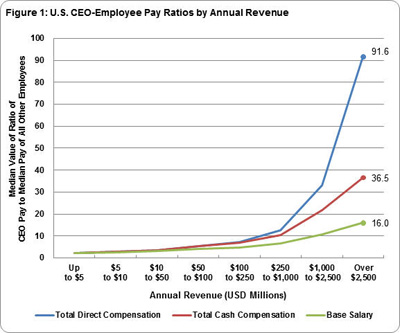

Figure 1 below illustrates how the difference in pay between CEOs and other employees increases exponentially for companies over $100 million in revenue. The opportunity for CEOs to earn large cash incentives and equity awards magnifies significantly in large companies, particularly for large public companies with complex global operations.

The median CEO-to-employee pay ratio for companies over $2.5 billion in revenue was 16.0 for base salary, 36.5 for total cash compensation and 91.6 for total direct compensation. Companies in the 90th percentile had multiples of 19.4 for base salary, 63.8 for total cash compensation and 187.1 for total direct compensation.

The highest multiple exceeded 200 for total direct compensation. In other words, the total direct compensation for the CEO was 200 times larger than the median total direct compensation of all other employees in the organization.

Source: Culpepper Compensation Surveys U.S. Database, |

Other Factors that Impact CEO-to-Employee Pay Ratios

In addition to company size, there are numerous factors to consider that influence CEO-to-employee ratios, including industry sector, job mix and geographic location.

• Location. While company size is the predominant factor influencing compensation for executive jobs, location is the predominant factor influencing compensation for most non-executive jobs. This analysis revealed that companies with a majority of employees in locations with high labor costs (e.g., San Francisco, New York) had lower CEO-to-employee pay ratios than companies in geographic locations with lower labor costs (e.g., Salt Lake CIty, Indianapolis).

• Industry sector/job mix. The analysis did not reveal significant differences between technology and life science industries. However, it was found that many companies in other industries had higher CEO-to-employee pay ratios. This is primarily attributable to the fact that technology and life science companies employ a higher percentage of skilled professional workers with a higher average level of compensation.

For example, companies with a high percentage of low-paying jobs (e.g., call centers, manufacturing, retail) typically have higher CEO-to-employee pay ratios than companies with a higher percentage of high-paying jobs (e.g., biotechnology, software).

When using a statistic like the CEO-to-employee pay ratio, it is important to control for company size, geographic location, industry sector and mix of jobs. If you do not consider the impact of each of these factors carefully, it is difficult to draw accurate conclusions about this ratio and how it compares to other companies.

More Questions than Answers

As Culpepper dug deeper, more questions and concerns surfaced about other complex issues that impact the calculation, interpretation and use of the CEO-to-employee pay ratio emerged.

• What about the value of medical benefits? The SEC's definition of total compensation excludes company contributions to group health insurance premiums and health savings accounts. Medical benefits are a significant portion of most employees' total rewards package (compensation and benefits). Excluding the value of medical benefits inflates theCEO-to-employee pay ratio and distorts the true relationship between CEO and employee pay.

• Are employees outside of the U.S. included in the "all-employees calculations"? If so, how do you compare fairly and accurately companies that only have employees in the U.S. to multi-national corporations that have employees across countries? A variety of complex factors need to be considered to address differences between countries, such as cost of labor, cost of living, currency fluctuations, tax rates and government-provided benefits. Each of these factors could distort the calculation of a meaningful CEO-to-employee pay ratio.

• What about part-time employees? Are part-time employees included in the "all-employees calculations"? If so, how do you fairly and accurately compare companies that have a lot of part-time workers to companies primarily employing full-time employees? Do you calculate full-time equivalent pay rates for each part-time employee? Companies that do not calculate a full-time equivalent pay rate for part-time employees will have a higher CEO-to-employee pay ratio.

• What about independent contractors? Are independent contractors exempt from this calculation? How do you compare fairly and accurately companies with a low percentage of contract workers to companies that outsource a high percentage of low-cost labor to independent contractors and other companies?

Each of these issues needs to be addressed and considered carefully. Based on the SEC's tentative schedule, the rules for clarifying and implementing the CEO-to-employee pay ratio will be proposed in mid-2011.

Critics cry that this is a "political" ratio, not an "economic" ratio, with an objective to cap executive compensation and punish companies with "excessive" CEO compensation. A bill has been introduced to Congress to provide preferential income tax rates and government contracts to companies with CEO-to-employee pay ratios below a certain threshold.

A Loaded Statistic

In their current form, the rules defining how the CEO-to-employee pay ratiois calculated have the potential to favor companies with factors that create lower ratios. For example, the ratio will favor companies in geographic locations with higher labor costs, and those in industries with higher-paying jobs. And it will favor companies that outsource low-paying jobs.

As with any government-mandated financial reporting requirement, the CEO-to-employee pay ratiohas the potential to be manipulated, miscalculated and misinterpreted. Will companies "manage" their ratio to avoid public scrutiny and embarrassment? Will companies "manage" their ratio to qualify for lower tax rates or preferential treatment for government contracts? These are questions that remain to be answered.

W. Leigh Culpepper, CCP, GRP, CBP, is president and CEO of Culpepper and Associates Inc., which conducts worldwide salary surveys and provides benchmark data for compensation and employee benefit programs. Jeremy Greenup, CCP, is a research analyst at the firm. Eric Hurst, Ph.D., is a survey data analyst and statistician at Culpepper and Associates Inc.

Reposted with permission.

Source: Culpepper Compensation & Benefits Surveys, October 2010, www.culpepper.com.

Related SHRM Article:

SEC Proposes Rule to Disclose CEO-to-Worker Pay Ratios, SHRM Online Compensation, September 2013

Related External Articles:

Pay Ratio Disclosures Made Simple, Leonard, Street and Deinard, September 2013

Pay Ratio Rules are Coming, Benefits and Compensation with John Lowell (blog), August 2013

A Simple Solution That Made a Hard Problem More Difficult, New York Times, August 2013

Quick Links:

SHRM Online Compensation Discipline

SHRM Metro Economic Outlook reports

• Sign up for SHRM’s free Compensation & Benefits e-newsletter |

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.