Addressing Racial Inequities in Retirement Savings

Lower 401(k) contribution rates by Black employees are often overlooked

Marlo J. Gaal, SHRM-SCP, is chief talent officer at Chicago-based Ariel Investments, a Black-owned mutual fund investment firm. As businesses began prioritizing diversity, equity and inclusion (DE&I) strategies over the past 18 months, Gaal received inquiries from HR colleagues about "all things DE&I," save one at the heart of Ariel's business.

"To be honest, I have not gotten a direct request" on increasing Black investors' savings rates, Gaal said, although Ariel publishes an annual survey with Charles Schwab detailing Black investors' statistics and sentiments. The latest survey, conducted in December 2020 among 2,104 U.S. adults with $50,000 or more in household income, found that historical disparities remain pronounced, even when excluding low-paid workers. For instance:

- Dollar contributions. White 401(k) plan participants, on average, invested 26 percent more per month toward their retirement accounts than Black 401(k) plan participants ($291 versus $231).

- Loan-taking. More than twice as many Black 401(k) plan participants than white participants (12 percent versus 5 percent) borrowed money from their retirement accounts.

The findings reflect long-standing wealth disparities in the U.S. According to Federal Reserve Board statistics compiled in 2019, the median net worth for Black families was $24,100, for Hispanic families $36,050, and for white families $189,000.

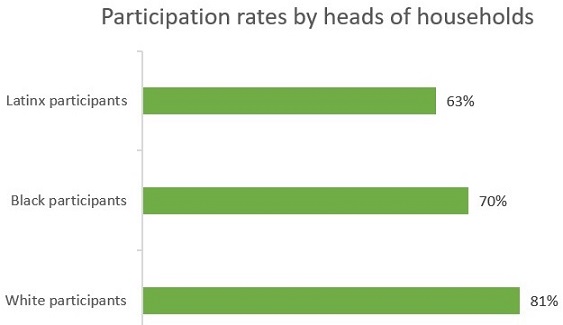

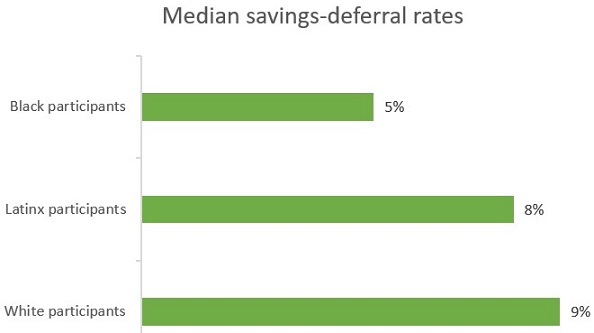

Racial Inequities in 401(k) Savings: Another View T. Rowe Price's Retirement Savings and Spending Study highlights racial disparities in 401(k) plan participation and savings-deferral rates, based on 3,420 participants who responded to a June 2020 survey. Among employees with access to a 401(k) or similar defined contribution plan at work, the survey showed: Source: T. Rowe Price, Retirement Savings and Spending Study (2021). "Better understanding the challenges underrepresented groups face can help employers and financial professionals develop strategies to help ensure participants of all races and ethnicities thrive financially and retire successfully," said Dee Sawyer, head of individual investors and retirement plan services at T. Rowe Price. |

Taking a Broad Approach

Gaal advised HR leaders to take a broad look at what they can do to help employees save, bearing in mind the challenges faced by members of communities that have been historically disadvantaged. Ariel, for instance, completely funds employees' health insurance premiums, freeing up more of the workers' paychecks for other allocations. Emergency savings accounts are also becoming more common as an employee benefit.

"There's no magic bullet," Gaal said. "HR executives, along with their [C-suite] peers, need to assess [workforce] demographics, your industry, what you can afford, and put a plan in place that makes sense for your organization."

Kezia Charles, director of retirement at consulting firm Willis Towers Watson, sees a new emphasis on DE&I efforts in retirement counseling planning. In a recent post on the Willis Towers Watson blog, Charles outlined steps employers can take to ensure DE&I in retirement planning is adequately addressed, such as:

- Measuring plan data and analyzing metrics by diverse cohorts. Look for low deferral rates, missed employer-match opportunities, loans, withdrawals and wage garnishments to highlight segments of the population that are more likely to have long-term financial insecurity.

- Reviewing plan design and access to it. According to Willis Towers Watson's October 2020 Global Benefits Attitudes Survey of 4,898 U.S. employees at large organizations, 48 percent of Black employees said they live paycheck to paycheck, compared with 37 percent of white employees. Employers should take the ability to save into account when evaluating plan design features—for example, if they contribute only through a matching feature, they should consider including a non-elective component.

- Evaluating the impact of pay on employees' ability to save. Black workers are 30 percent more likely than white workers to earn less than $50,000 annually, according to the Bureau of Labor Statistics, and white workers are five times more likely than Black workers to earn $200,000 or more. Employers hoping to address savings gaps should review pay practices.

- Considering tools and resources to improve financial resilience. Employers can provide access to financial planners, especially for employees who apply for loans or withdrawals from their savings.

Charles also noted that some employers are considering including options such as lifetime annuities in their plans. "As employers think about things like lifetime annuities and lifetime income, we'll continue to see innovation in the market," she said.

Mike Webb, an institutional financial advisor with Captrust in New York City, said employers that automatically enroll employees in a 401(k) plan and automatically notch up participants' savings rates annually "can help mitigate differences in minority savings rates over time." That's backed by a 2011 study by Vanguard Investments, which showed auto-enrolling Black and Hispanic employees raised their participation rates by more than 60 percent and 40 percent, respectively.

Redefine 'Defined Contribution'? "The 401(k) is really working pretty effectively for high earners," said Kathleen Houssels, founder of Aspire Ten25 in Danville, Calif., a firm specializing in environmental, sustainable and governance (ESG) investing strategies. "The lower end of the spectrum is struggling, and people are relying more and more on Social Security to get by." Houssels and Steve Dean, chief investment officer of the Claraphi Advisory Network in Aliso Viejo, Calif., recently co-authored a paper that proposes a shift in employers' approach to investing in employees' 401(k) accounts. They suggested, for instance, that employers contribute $2,000 annually to employee accounts instead of a percentage match, and to make that contribution directly to a target-date fund with some exposure to higher-risk/higher-reward stocks. Ariel's founder, John Rogers, noted in remarks to CNBC that Black investors have historically chosen the most conservative investment options. Automatically allocating the employer's contribution to a target-date fund, rather than relying on a participant's fund choice, could help retirement accounts grow faster, Houssels and Dean believe, allowing even lower-income families to amass $500,000 in wealth over the course of a career. |

Cultural Compatibility

Rebecca Liebman, CEO of Boston-based LearnLux, which offers personalized fiduciary advice through a digital platform, referred to research from the Employee Benefit Research Institute's latest retirement confidence survey, which showed clear cultural differences in the way various ethnic groups regard prioritizing retirement savings. For example, high-income Black workers and Hispanic workers of all income levels believed it is more important to help friends and family now than to save for their own retirement.

"The traditional advice of maxing retirement savings runs counter to what's taught culturally," Liebman said. "People are more likely to follow a financial plan if they work with somebody who understands them and who they trust. And many times that means they want to work with somebody who has been through the same life experiences or cultural events."

Currently, however, financial advisors do not represent the demographics of the United States—just under 2 percent of certified financial planners (CFPs) are Black, Barron's reported earlier this year.

Liebman said LearnLux is committed to increasing the diversity of its own CFPs and has established a scholarship for those from traditionally underrepresented demographic groups who wish to become CFPs.

Ariel's Gaal said HR managers should ensure useful information is readily available for every employee cohort, and to "leverage the relationship with your 401(k) administrator … to help you get the word out."

Houssels also said communications are vital, and that employers can prime the pump by front-loading employees' accounts and having something tangible to communicate about.

"Our strong belief is, the best way to start the process is [to] provide some retirement savings for people and educate them along the way," she said. "When employees can see what's happening in their accounts—how the money is growing—that's an easier conversation than trying to convince somebody up front to take 5 percent of their salary and put it away."

Greg Goth is a freelance health and technology writer based in Oakville, Conn.

Related SHRM Articles:

Minority Wealth Gap Isn't Just About Income, SHRM Online, October 2021

Black Workers Still Earn Less than Their White Counterparts, SHRM Online, June 2020

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.