Helping Employees Save for the Unexpected Pays Off

Rainy day accounts and discount programs can keep workers solvent

A survey from the U.S. Federal Reserve garnered attention when findings showed that a significant portion of the population would be unable to pay for a $400 unexpected expense outright. The survey, conducted in October and November 2018, also showed that 17 percent of adults are not able to pay all of their current month's bills in full, and 12 percent would be unable to pay their current month's bills if they also had to pay for an unexpected $400 expense.

Individuals who are this cash-strapped may have to resort to extreme measures in even the most mundane circumstances. The survey, known as the Survey of Household Economics and Decisionmaking, found that 27 percent of the 11,440 respondents would borrow or sell something to meet an unexpected $400 expense, and 12 percent would not be able to cover the expense at all.

HR executives have likely encountered employees in similar circumstances. These employees often have their wages garnished, rely on high-interest payday loans and borrow against any retirement savings they might have accumulated.

This is why Dawn Food Products helped its approximately 5,000 employees with unexpected expenses. The effort began with negotiating discounts with retailers on big-ticket items, such as major appliances, that employees could pay for via payroll deduction, according to Brian Coleman, the Jackson, Mich.-based company's vice president of total rewards. Following the program's launch, "the number of 401(k) plan loans employees took out fell by 3 percent, while employee 401(k) contributions increased from 5 percent to 7.5 percent," Coleman said. "I attribute those results to the discount program."

Recognizing that employees might need help paying for other types of emergency expenses, such as a major car or home repair, the company recently began offering a payroll deduction that allows employees to make after-tax contributions to a rainy day fund. Although only about 25 employees signed up in the first few months, Coleman is confident that the program will take hold once the company launches its communication initiative. The company plans to use the results of the Federal Reserve study to talk about the importance of emergency savings.

Encouraging Rainy Day Savings

SunTrust Banks, which administers emergency savings accounts for employers, analyzed its client data and found that 32 percent of companies offer employees a financial incentive to save, often linked to the employee's participation in programs that teach skills such as how to create a budget and spend within it.

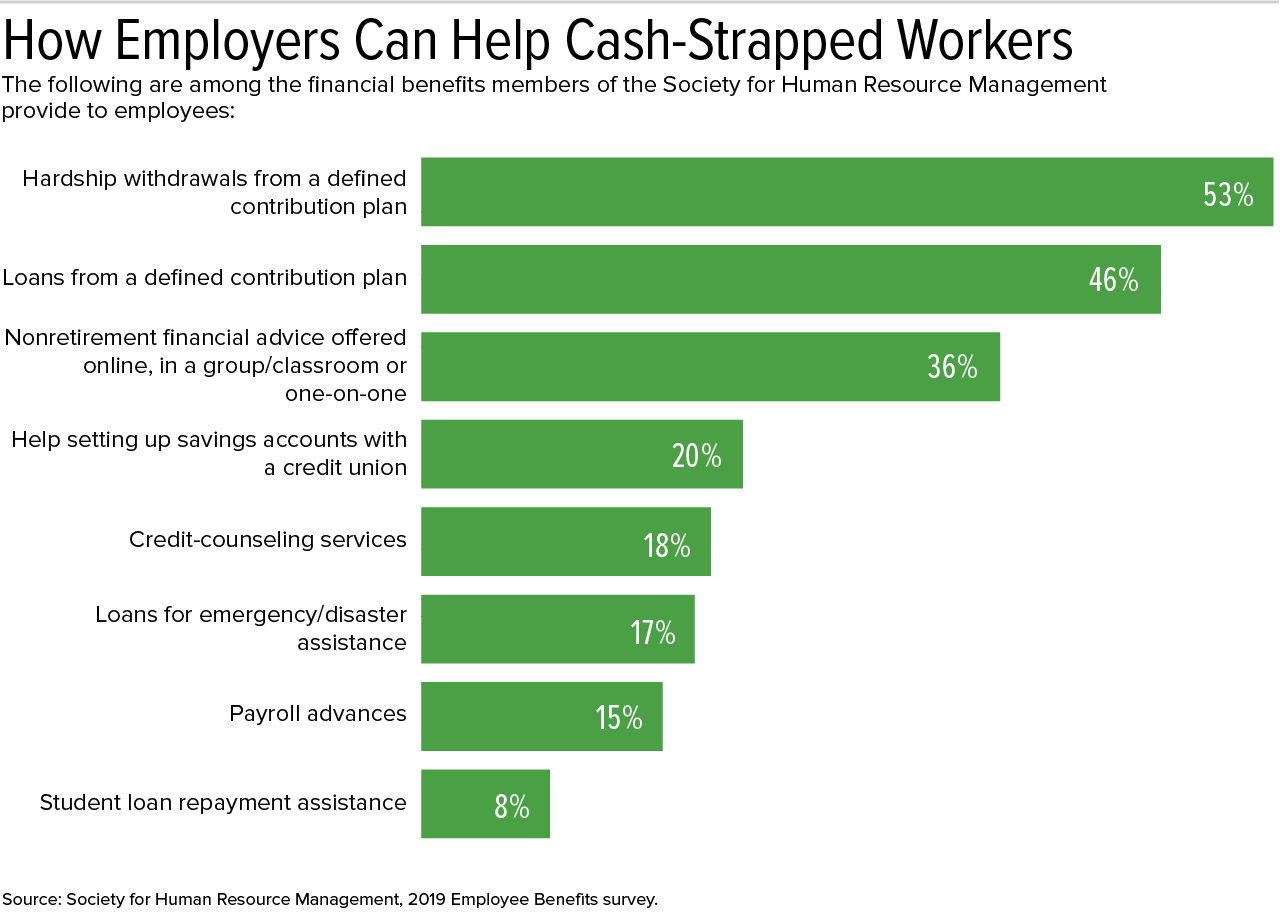

According to the Society for Human Resource Management's 2019 Employee Benefits survey, which received responses from 2,763 HR professionals, 36 percent of respondents said their organization offers nonretirement financial advice to employees delivered online, in a group or one-on-one, and 20 percent help their workers set up savings accounts with a credit union.

SunTrust offers to deposit $1,000 in its employees' emergency savings accounts if they complete the company's financial wellness program, according to Brian Nelson Ford, a financial well-being executive with SunTrust in Atlanta. Employees receive $600 in a lump sum, with the remaining $400 deposited in the employees' accounts over the course of a year.

Such incentives are likely to get employees' attention, especially those most in need of an emergency savings account. A 2018 survey of 2,603 adults between ages 25 and 64, conducted by AARP and Boston Research Technologies, found that while 71 percent would likely participate in a payroll-deduction rainy day savings program if their employer offered one, 87 percent said they would be more likely to open such an account if their employer matched their contributions.

The survey also found that neither household income nor retirement account balances had much of an impact on participation in emergency savings initiatives. Instead, financial stress and the amount of nonretirement savings people have are key indicators of interest in an emergency savings account. For example, 80 percent of the respondents who are very or somewhat stressed about their finances would be very motivated to use these accounts, as would 82 percent of those with less than $2,000 in nonretirement savings and 77 percent of those with $2,000 to $10,000 in savings.

Ford noted that incentives are important, but "the size of the incentive is not as important as some people think." An organization with a limited budget can get employees' attention with a relatively nominal amount, such as a one-time contribution of $100. "In companies with a certain culture and generally higher levels of pay, a larger incentive may be necessary to motivate participation," he said.

Monroe, N.C.-based home builder True Homes has also tied emergency-fund incentives to participation in its financial fitness program.

"Once employees complete the initial modules of the financial wellness program, the company provides them with $250 that they can use to start an emergency fund," said Les Gleaves, the company's executive partner for organizational development.

So far, 40 percent of the workforce has been eligible for the offer, Gleaves said.

[SHRM members-only toolkit: Managing Employee Assistance Programs]

Measuring Up

Once emergency savings accounts are in place, employers can gauge their effectiveness by looking at certain metrics such as program participation levels, amounts contributed and average account balance.

"If you are not getting to participation levels of 20 percent to 40 percent [in the company's emergency savings program], you are probably not reaching the people who need these accounts the most," said Ford.

Employers can also compare broader metrics before and after initiating the savings program, such as the number and size of 401(k) loans taken out and wage garnishment levels. Any improvement on any of these metrics likely means that employees are becoming better prepared to deal with life's financial emergencies with less financial stress.

Joanne Sammer is a New Jersey-based business and financial writer.

Related SHRM Articles:

Employers Feel More Responsible for Employees' Financial Wellness, SHRM Online, October 2020

Emergency Savings Accounts Funded by Payroll Deductions Boost Financial Wellness, SHRM Online, September 2020

How Income-Advance Loans Help Financially Stressed Employees, SHRM Online, February 2020

Financial Wellness Perks Expand to Address Employee Needs, SHRM Online, June 2018

Tying Health Plan Premiums to Salary Can Aid Lower-Paid Earners, SHRM Online, October 2017

Reach Out to Workers Living Paycheck-to-Paycheck, SHRM Online, September 2016

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.