6 Ways to Measure the Success of Financial Wellness Efforts

Employers are missing out on opportunities to improve these programs

Financial wellness programs, such as those that promote savings and teach household budgeting skills through online or group instruction, are proliferating as employers invest in efforts to help workers manage their finances. However, only 30 percent of employers measure the effectiveness of these offerings, according to a 2018 study of 657 employers conducted by Bank of America Merrill Lynch.

Without those measurements, employers may be missing out on opportunities to improve these benefits and may not even have a clear idea of what they want to achieve by offering them, such as reducing employees' money-related stress so they can be more productive at work.

Finding the Right Metrics

The challenge in measuring such programs is defining what they mean for the organization. In terms of less employee stress, for instance, should employers focus on the financial return on the investment? Is financial wellness part of a larger strategy to enhance the organization's brand in the view of current and prospective employees? Or is the focus on improving employees' lives, whether or not that improves their job performance?

To help organizations answer these questions, benefits advisors recommend that employers focus on these six metrics.

1. Use and engagement.

Financial wellness programs won't make much difference if employees aren't using them. By relying on vendors' data, employers can track the number of workers signing up for financial wellness offerings, completing tutorials and related activities, and taking measurable steps toward better financial management.

2. Benefits and payroll data—positive indicators.

Employers can use data from their employee benefits plans to check up on employees' financial health. Increased enrollment in and contributions to retirement plans, automatic savings programs and health savings accounts (HSAs) can indicate that employees have extra money to save and invest for future needs.

The number of employees contributing the maximum to retirement plans and HSAs may indicate that financial wellness programs are having a positive effect, as can the number of employees taking advantage of employer-sponsored group life, disability and other safety net coverages.

3. Benefits and payroll data—negative indicators.

Payroll and 401(k) plan data on the number of outstanding 401(k) loans, the frequency of 401(k) hardship withdrawals and loan defaults, and the number of emergency or payday loans can help employers understand the level of financial hardship employees are experiencing. The number of, frequency of and reason for pay garnishments is also important. "People with manageable debt have fewer or no garnishments," said Laurie Brednich, CEO of HR Company Store, a Chandler, Ariz.-based website that helps HR professionals find vendors. "If many of these garnishments are for medical expenses, perhaps a company needs to revisit their benefit plan designs."

[SHRM members-only how-to guide: How to Design an Employee Benefits Program]

4. Turnover.

It is difficult to draw a straight line between employee retention and financial wellness, but that doesn't mean employers shouldn't try to track the connection between the two. "While no single wellness benefit drives retention, holistically, wellness benefits show your company cares—and that does drive retention," said Carla Dearing, CEO of Sum180, a mobile financial wellness services provider based in Louisville, Ky.

5. Absenteeism, productivity and health care costs.

Lack of financial well-being can increase employees' stress and on-the-job distraction. Data on disability and workers' compensation claims, as well as on health benefits claims for stress-related illnesses, can help employers measure the results of financial wellness benefits.

Similarly, "tracking absenteeism rates over 18 to 24 months among program participants versus nonparticipants can give employers a sense of how a particular financial wellness program is working to reduce employee stress," said Chris Whitlow, CEO of financial wellness platform Edukate in Orlando, Fla.

6. Front-line feedback.

Employees and front-line managers can tell HR whether and how workers are benefiting from financial wellness efforts—if HR asks. Employees and managers can also help organizations understand how those programs may not be resonating with the workforce. "[HR could] reach out to supervisors and ask how many people are requesting overtime consistently," Brednich said. "Employees who frequently request overtime usually want the extra money to pay down debt."

Employers can gather some of this data themselves, but they should also request data from financial wellness vendors and, as appropriate, from health and retirement benefits providers.

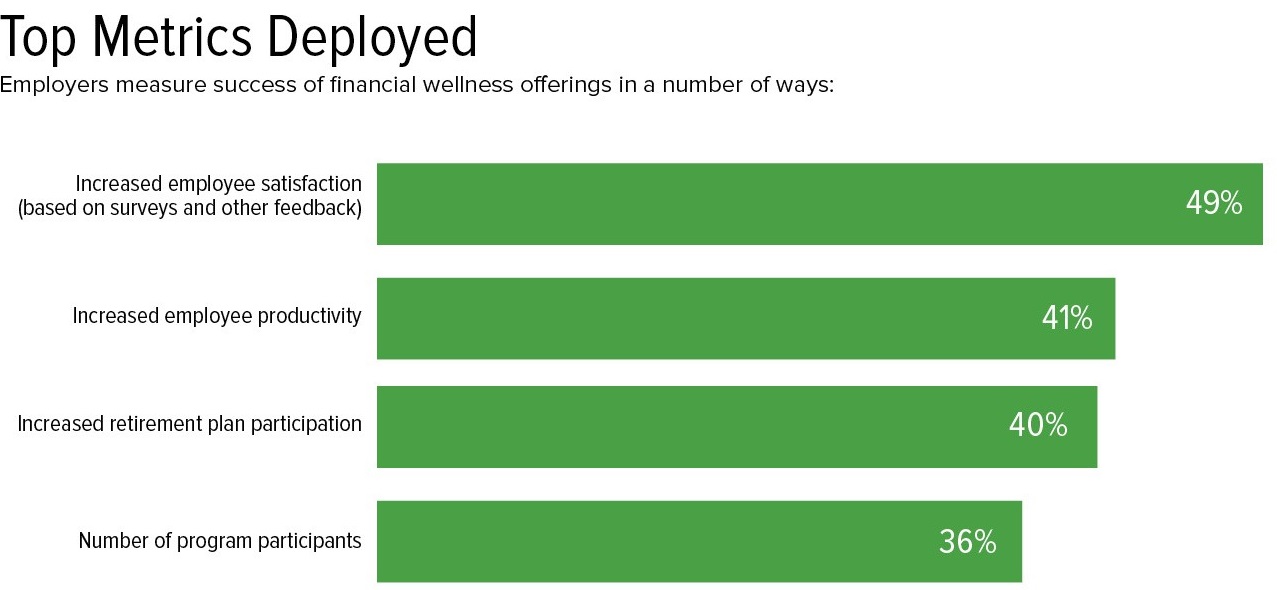

Source: Benefits and Beyond: Employer Perspectives on Financial Wellness, a Prudential Financial report. The fall 2017 survey received responses from 777 U.S. businesses with at least 100 full-time employees.

'Holistic' Offerings Yield Greater Value

"Even defining what is meant by financial well-being and what constitutes financial wellness initiatives can be challenging," said Lori Lucas, president and CEO of the nonprofit Employee Benefit Research Institute (EBRI) in Washington, D.C.

Core features of a financial wellness program typically include help with managing credit card loans, budgeting tools and financial counseling. In a 2018 EBRI survey, employers cited plans as varied as employee discount programs, student loan repayment subsidies and emergency savings accounts as part of their arsenal of financial wellness initiatives.

Employers that offered holistic (meaning ongoing and multifaceted) financial wellness programs rather than periodic campaigns or one-time initiatives were more likely to try to raise employees' appreciation of their benefits, according to EBRI's Financial Wellbeing Employer Survey, which was conducted in July 2018 with responses from 250 full-time benefits decision-makers at companies with at least 500 employees.

Employers cited a wide range in costs for their financial wellness initiatives, with 43 percent reporting the annual cost per employee as $50 or less. But employers offering holistic programs spend more to achieve more, with 21 percent of these employers citing an average annual cost per employee of more than $500.

"Because employers are generally footing the cost for these programs themselves, they want to be able to demonstrate that the programs are effective," Lucas said. "Once the pilot or one-off program is implemented, we're hearing that the key is to demonstrate its success so that it can be made more broadly available."

EBRI found that at 80 percent of the employers surveyed, an HR professional was either a primary or secondary champion of introducing financial wellness initiatives.

Joanne Sammer is a New Jersey-based business and financial writer. Stephen Miller, CEBS, contributed to this article.

Related SHRM Articles:

The 10 New Benefits Workers Want, SHRM Online, December 2018

Financial Wellness Perks Expand to Address Employee Needs, SHRM Online, July 2018

How Improving Financial Health Boosts Productivity, SHRM Online Benefits, December 2017

Take a Team Approach to Financial Wellness, SHRM Online, October 2017

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.