401(k) Savings Rates Are Up, and SECURE Act May Push Them Higher

Automatic enrollment and auto-increase features drive retirement readiness

Thanks to the Setting Every Community Up for Retirement Enhancement (SECURE) Act, signed into law at the end of 2019, employers offering a safe harbor 401(k) plan with an automatic increase (or auto-escalation) feature can raise plan participants' contributions until they amount to 15 percent of pay, unless participants opt out of these increases. Before the SECURE Act was passed, the cap on default contributions under an auto-escalation program was 10 percent for safe harbor plans.

Higher default contribution rates can prod workers to save more for retirement—if they can afford to do so.

Once participants in safe harbor plans are contributing 15 percent of their paycheck, auto-escalation ends—although employees can choose to increase their savings rate above 15 percent.

Under the SECURE Act, this change is effective for 401(k) plan years beginning Jan. 1, 2020. The law stipulates that the 10 percent cap still applies through the plan year that begins after the employee's date of participation, and then the cap goes up to 15 percent for subsequent plan years.

"Overall, the amount people are saving is starting to ratchet up," said David Reich, national president of retirement services for global insurance brokerage Hub International. "But for people to be better positioned for retirement, it really needs to be 10 percent at a minimum and closer to 15 percent" on average throughout an employee's career.

"Getting people there is the issue," he added. "The SECURE Act will help in a big way."

A 10 percent cap may "sound like it's going to be sufficient when you're bringing employees in at a very young age," said Jack VanDerhei, director of research at the nonprofit Employee Benefit Research Institute. However, "when you've got midcareer hires who unfortunately may not have had any coverage previously, or who may have cashed out those amounts, then having the ability to get those people escalated up to 15 percent is going to be extremely important."

John Lowell, an actuary and advisor with October Three Consulting, called the new 15 percent threshold one of the most significant reforms in the new law, but he added that he wonders how many eligible employees would decline an automatic deferral increase above 10 percent of their pay.

Alan Vorchheimer, a principal with HR advisory firm Buck, wrote that raising the cap on auto-escalation in safe harbor plans is a positive change, but "it also sends a message to participants that this is the preferred way to save without explaining the alternatives." For instance, employees who decide to divert more of their paycheck to their 401(k) may do so at the expense of their health savings account or even a Section 529 tuition assistance plan from which, under the SECURE Act, the balance can be used to pay down student loan debt.

Vorchheimer suggested, "[You] may want to consider how you can help participants maximize what is available rather than expecting them to navigate all the options for tax-advantaged savings themselves."

Safe Harbor Plans Only

While the SECURE Act raises the cap on automatically increasing payroll deferrals in safe harbor plans, there is no limit on automatic deferral rates for non-safe-harbor plans, Meghan Murphy, vice president of Fidelity Investments, pointed out.

Safe harbor 401(k) plans are exempt from annual nondiscrimination tests used to determine if the plans are used disproportionately by highly compensated employees (HCEs). If HCEs defer more than other employees by more than a certain amount, the plan will fail nondiscrimination testing and must refund deferrals to the HCEs.

As of the end of 2019, 70 percent of Fidelity's 401(k) clients had safe harbor plans, Murphy said.

Savings Rates Are Up

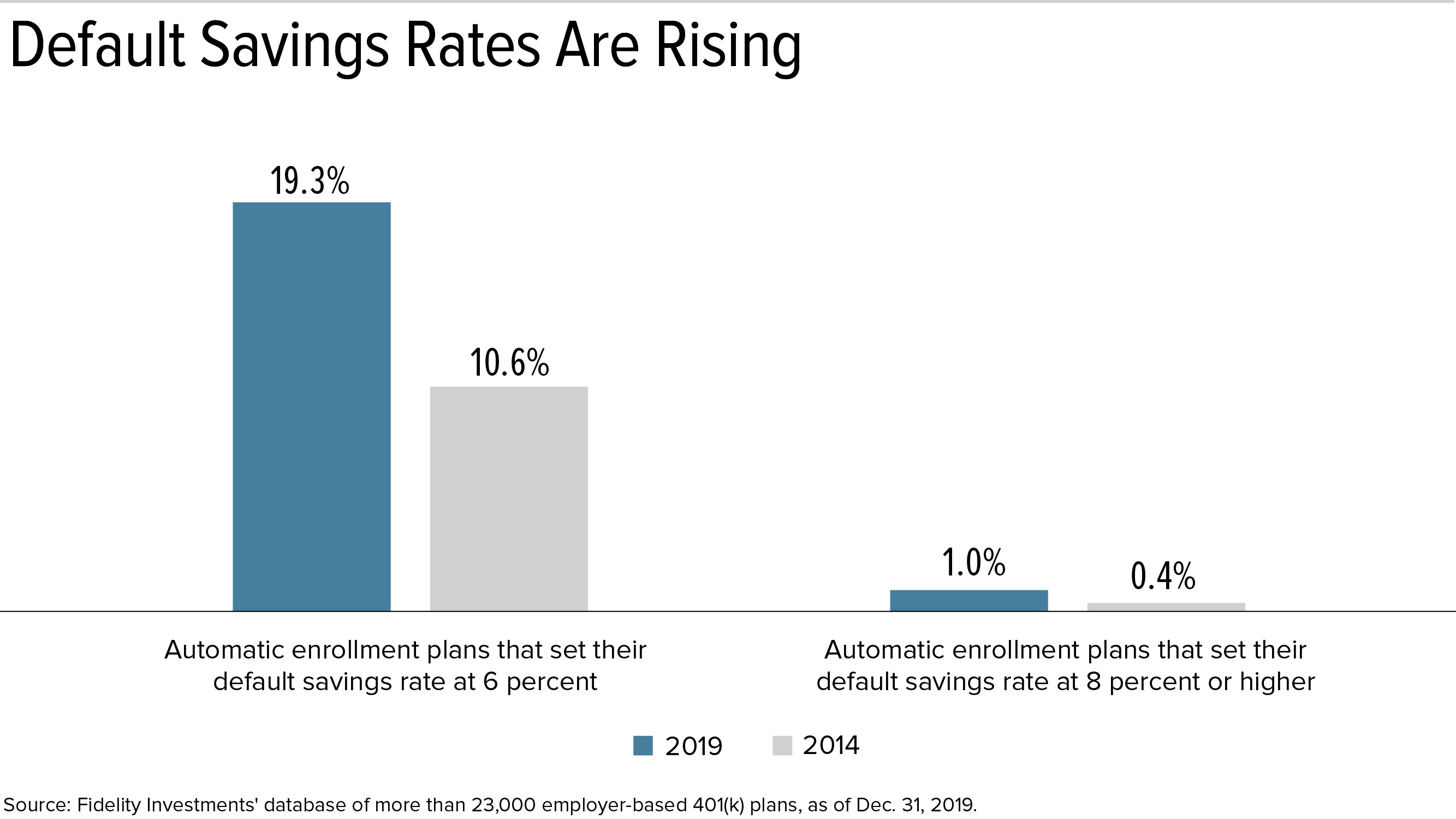

"We've seen a trend over the last several years of employers moving away from a 3 percent automatic default rate to higher rates," Murphy noted. "Today, 34 percent of employers are auto-enrolling at a 5 percent or higher default deferral, versus 19 percent that did so five years ago."

In addition, "those defaulting at a 6 percent rate have doubled in five years" to 19.3 percent from 10.6 percent, Murphy said. "Those defaulting at 8 percent or higher have doubled over the last five years" to 1 percent from .4 percent.

Those figures are based on recordkeeping services that Fidelity provides for roughly 23,000 employer-based 401(k) retirement plans and reflect plan-design features as of Dec. 31, 2019.

Among Fidelity clients, the median automatic default savings rate is 4 percent of pay, but "an 8 percent default rate is no longer uncommon," Murphy said. "Employers are really looking at 'what can I do to help get my employees on the right track?' "

Fidelity's data further shows that for 401(k) savings overall:

- The median savings rate has been increasing steadily and is now 10 percent of pay, which is an improvement over 2018 levels of 8.8 percent and up significantly from 3.6 percent in 2006.

- Baby Boomers saved the most, stashing away 11.7 percent of their salaries, an increase from 9.9 percent in 2018.

- Millennials also increased their median savings rate, improving to 9.7 percent going into 2020 from 7.5 percent in 2018. Their 401(k) contributions are now on par with Generation X, whose savings rates are up from 8.6 percent in 2018.

Despite this, all savings levels are still well below Fidelity's suggested total savings rate of at least 15 percent, which includes employer contributions.

"Most people don't start out early in their career being able to save 15 percent in total, which may mean that later in their career they need to save upwards of 18 percent, 19 percent or 20 percent to make up for it," Murphy noted. "Saving just 1 percent or 2 percent more each year really goes a long way, especially over the length of their career."

A positive sign: One-fourth of Millennials are saving 15 percent or more of their pay, including employer matching contributions, Murphy said. "It's fascinating to see them taking responsibility for their retirement readiness at a young age."

Default Rates and Escalation Caps Vary

In deciding where to cap the default savings rate, initially with automatic enrollment and then through auto-escalation, "consider your employees' ability to save at a higher rate, as well as what their retirement readiness looks like," Murphy advised.

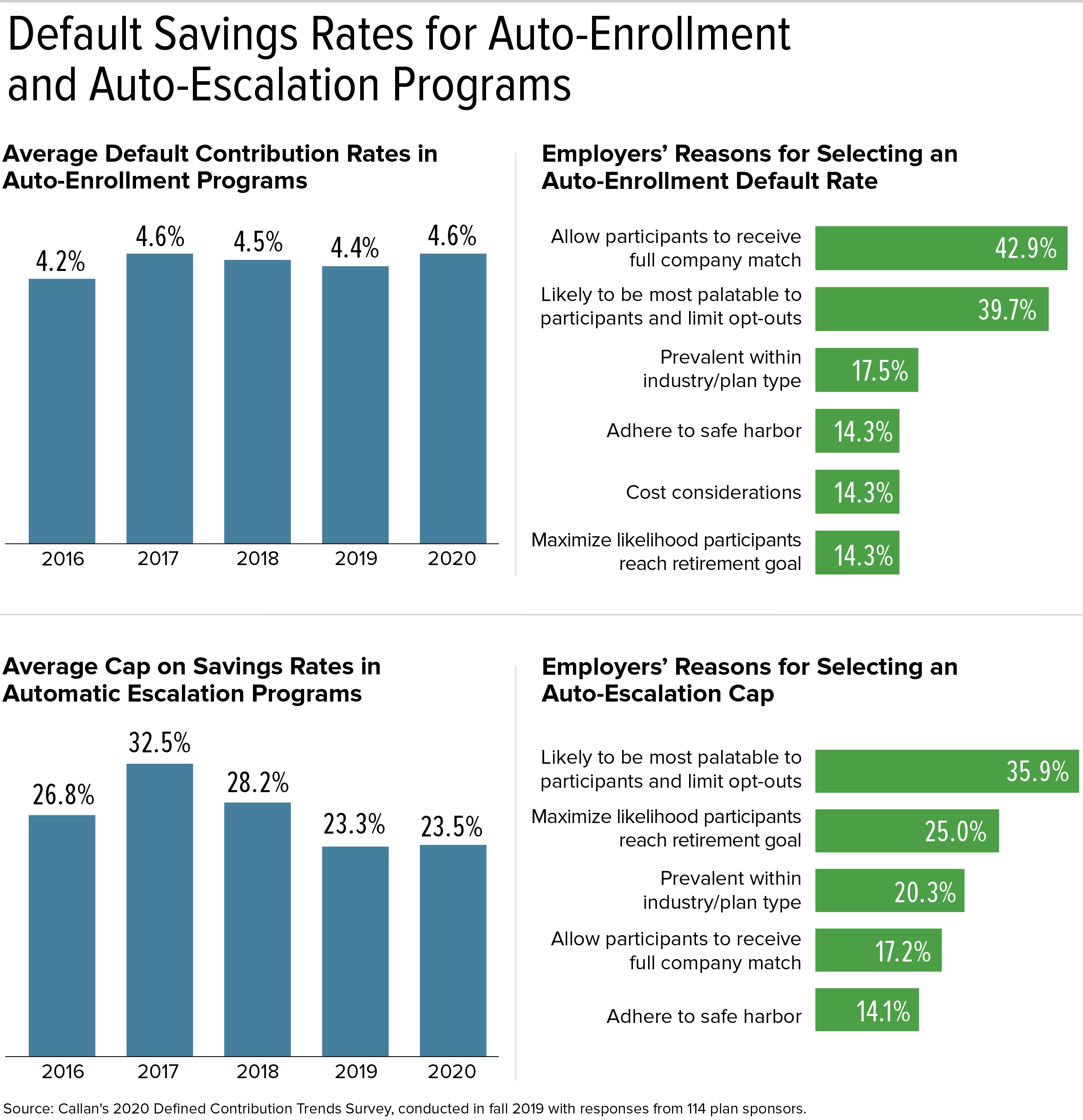

According to the Callan Institute, an institutional investment firm, last year default contribution rates for automatic enrollment typically ranged from 1 percent to 8 percent of participants' pay. The average default deferral rate held steady at 4.4 percent, with a median rate of 4 percent. (Outliers, or extreme values on either the high end or low end of a contribution range, have a bigger effect on the mathematical average than on the median, which is the middle value in a list ordered by size.)

Callan conducted its 2020 Defined Contribution Trends Survey last fall, which fielded responses from 114 mostly large plan sponsors.

Callan found that, as in prior years, plans with an automatic escalation feature usually raise plan participants' contributions (unless they opt out) annually by 1 percent of pay—93 percent of survey respondents reported this level, while the rest used a 2 percent auto-escalation rate.

The average cap on auto-escalation default savings rates in 401(k) plans, including non-safe-harbor plans not capped by law, declined in 2019 to 23.3 percent of compensation, down from 28.2 percent in 2018, Callan found. The median cap remained steady at 10 percent, however.

"Automatic enrollment has seemingly reached saturation, remaining at around 7 in 10 plans for the past four years," said Jamie McAllister, senior vice president at Callan. "Of those that do not automatically enroll employees, 5.6 percent report that they are very likely to implement this feature in 2020," she noted.

Automatic Escalation Pushes Savings Higher

Roughly 72 percent of Fidelity clients have adopted an auto-escalation feature, Murphy said. "For 19 percent [of organizations], it's automatic with an option to opt out, and for the rest it's an option that employees can affirmatively select." Larger employers are more likely to embrace auto-escalation, she pointed out.

While about 35 percent of employers overall are offering automatic enrollment unless participants opt out, "it's much more popular among plans that have over 500 employees, with about 65 percent of large employers using it," Murphy said.

The small end of the market is less likely to use auto-enrollment and auto-escalation, Murphy explained, often because these employers are concerned their employees will resent it, or because it would mean spending more on matching contributions, which drives up plan costs for employers.

Higher costs is "certainly a concern we hear, but we also hear from employers that they can't get people to retire because they haven't saved enough," Murphy said. "Strategically, adding [automatic enrollment and escalation] to your plan increases the likelihood of employees being retirement ready."

Related SHRM Articles:

401(k) Contribution Limit Rises to $19,500 in 2020, SHRM Online, November 2019

Consider 401(k) True-Up Payments for Employer Matching Contributions, SHRM Online, October 2019

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.