How to Make Your Organization Retirement-Ready

With 10,000 Baby Boomers leaving the workforce every day (one represented by each dot above), business leaders can no longer afford to ignore the &r& word.

Introduction

Newport News Shipbuilding is facing some harsh business realities. Its workforce is made up mainly of two key demographics: highly skilled Baby Boomers with valuable experience—but an eye toward retirement—and a younger set of workers who have promise but often don’t stick around long enough to master the art of building nuclear submarines and aircraft carriers.

About half of the company’s 22,000 employees are over the age of 50, and 30 percent are eligible to retire within the next five years. “That’s sobering,” says Susan Jacobs, vice president of human resources and administration for Newport News Shipbuilding, a division of Huntington Ingalls Industries, based in Newport News, Va. “We needed to get more serious about it.”

This year, the company is initiating a formal program to entice experienced workers to mentor younger employees and pass along knowledge gleaned over their lengthy careers. Informal methods of transferring knowledge have been in place for years, but company leaders wanted to develop a more deliberate approach. Being able to document processes and procedures is crucial to the business’s future success. “You can’t learn shipbuilding at school,” Jacobs says, noting that fostering personal connections between employees at all levels may have the added benefit of lowering attrition among younger workers.

This year, the company is initiating a formal program to entice experienced workers to mentor younger employees and pass along knowledge gleaned over their lengthy careers. Informal methods of transferring knowledge have been in place for years, but company leaders wanted to develop a more deliberate approach. Being able to document processes and procedures is crucial to the business’s future success. “You can’t learn shipbuilding at school,” Jacobs says, noting that fostering personal connections between employees at all levels may have the added benefit of lowering attrition among younger workers.

Newport News is hardly the only organization facing a “brain drain,” as an estimated 10,000 Baby Boomers leave the workforce each day. The exodus is forcing many companies to devise strategies to help employees retire while ensuring that operations don’t suffer as a result.

Heading for the Exits

Ensuring the stability of the business and guiding employees toward retirement is a complicated endeavor for a multitude of reasons, not the least of which is that retirement is a taboo topic in many workplaces. Managers often dread bringing it up for fear of being perceived as ageist. And employees are loath to ask about it because they don’t want to be seen as just biding their time until they can leave.

“This is not a subject people want to talk about,” says Catherine Collinson, president and chief executive of the Transamerica Center for Retirement Studies and the Transamerica Institute. “There’s a big disconnect between what employees want and what employers want.”

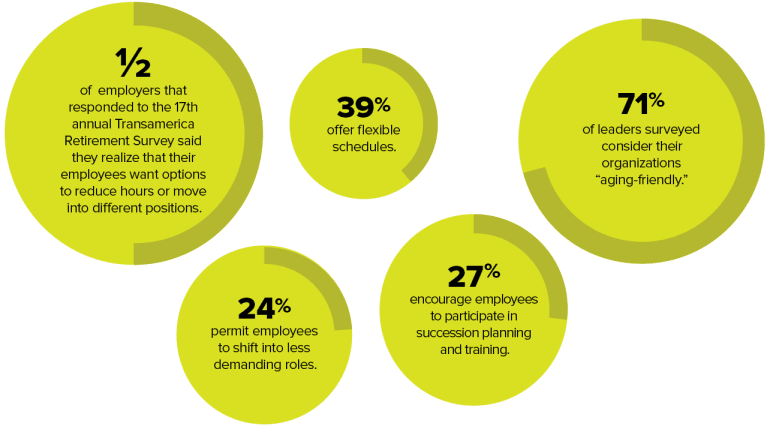

Research bears this out. Almost half of 1,802 employers that responded to the 17th annual Transamerica Retirement Survey said they realize that their employees want options to reduce hours or move into different positions. Yet only 39 percent offer flexible schedules, and 24 percent permit employees to shift into less-demanding roles. Only 27 percent of the organizations encourage employees to participate in succession planning and training. Nonetheless, 71 percent of leaders surveyed consider their organizations “aging-friendly.”

The Great Recession granted executives a reprieve from thinking about how Baby Boomer retirements would affect them because many workers had no choice but to stay put amid the market meltdown that decimated their savings.

“The recession just refocused everyone’s priorities. Now, people are beginning to talk about retirements again,” says Jacquelyn B. James, co-director of the Boston College Center on Aging & Work.

An improving economy and rising stock market appear to be affecting Baby Boomers’ attitudes about working. According to the results of a recent Gallup Economy and Personal Finance survey, by a ratio of more than 2-to-1, respondents said they are working because they want to and not out of financial necessity.

There is also evidence that companies are playing more-active roles in preparing their employees for retirement. Many business leaders believe it is in their best interest to help older workers become fiscally stable, since financial stress leads to lower productivity in the short term and could prompt workers to delay retirement even if they become disengaged in the long run. This year marks the 40th anniversary of the regulation that created the 401(k), which allows employees to set aside income for future use. Today, 90 percent of employers offer their workforces access to financial wellness programs, which include information on how to manage debt, create budgets and plan for retirement, according to a survey report from Fidelity Investments and the National Business Group on Health. That’s up from 84 percent in 2017.

The HR team at Newport News introduced a financial wellness program last year after learning that many of its employees weren’t contributing to its 401(k) plans and that those who did weren’t saving much.

“You don’t want to have people be in a situation where they want to retire but they can’t afford to,” Jacobs says.

How to Get Retirement-ReadyDefine what you want to elicit from employees. Are you trying to get long-term employees to stay full time? Part time? As mentors? Do you want to make it easier for them to leave? Determine your organization’s goals. Extensively survey all levels of the corporate hierarchy. Conduct focus groups to delve deeper into the company’s needs and employees’ mindsets. Make sure senior executives are committed to the plan. Changes will be enacted more easily if employees understand that management considers the policies a priority. Promote the plan vigorously. Put up banners in the office. Hold educational meetings. Older employees may be reluctant to work part time because they worry the decision might be held against them. Send clear signals that it is OK. Be specific. Outline exactly who is eligible for each program to avoid conflicts and misunderstandings. If you opt to offer phased retirement for only certain segments of the workforce, for example,explain the rationale to everyone. Conversations about age and retirement are fraught with potential liability issues. Choose your words carefully. |

Shortages Ahead

Guiding employees on the road to retirement is more challenging in industries with older workforces and labor shortages, such as shipbuilding, defense, manufacturing, utilities and health care.

The skills gap in the manufacturing sector will cause 2 million jobs to go unfilled in the decade ending 2025, according to a 2015 report by Deloitte and the Manufacturing Institute. During the same period, 2.7 million Baby Boomers are set to retire from manufacturing jobs.

The average U.S. manufacturer may lose an estimated 11 percent of its annual earnings—or $3,000 per existing employee—due to talent shortages, the report found.

Moreover, younger workers may be disinclined to fill the same roles of their older colleagues. At Newport News Shipbuilding, for example, “they don’t want to learn to build ships,” Jacobs says. “They want to build apps.”

Baby Boomers make up about 34 percent of the 5,000 U.S. employees at Herman Miller, an office furniture manufacturer based in Zeeland, Mich. The company implemented a phased retirement program in 2012 to entice older workers to stay on the job.

“We are in a tight labor market and have to work to keep good talent,” says Kim Smit, HR performance accountability project manager at Herman Miller.

Employees who are at least 60 years old and have been with the company for at least five years can cut back to between 20 and 32 hours a week in exchange for helping younger colleagues learn the ropes. They can stay in the program for six months to two years, giving the organization ample time to replace them or rethink the requirements of the position. Program participants can continue to purchase their health care through the company at the same rate as full-time staffers.

There was some initial pushback from managers who didn’t want the hassle of rearranging work schedules. Also, some employees were confused about how a reduced workload would affect benefits such as paid vacation. And while Smit says it’s difficult to quantify the program’s financial benefits, she cites the high marks it has garnered in employee surveys. “It’s great for morale,” she says.

Leaders at Herman Miller have long provided employees with counselors to help them manage their money and prepare financially for retirement. This year, the company will introduce a pilot program designed to address the emotional side of preparing for a life change.

“There is this existential phase in retirement where people start thinking, ‘What am I going to do now?’ ” explains Deb Vos, employee benefits manager at Herman Miller. “We want to provide a softer, gentler way to ease into retirement.”

Planned Departures

HR leaders at Bon Secours Virginia Health System in Richmond, Va., have implemented policies intended to insulate the organization from the health care industry’s endemic labor shortages. A 2015 report from the Association of American Medical Colleges predicts a deficit of anywhere from 46,100 to 104,900 doctors by 2030. And a 2015 study by the Georgetown University Center on Education and the Workforce found that the U.S. will face a shortfall of 193,000 nurses by 2020. Baby Boomers currently make up more than 1.1 million nursing professionals, accounting for more than one-third of registered nurses, licensed practical nurses and licensed vocational nurses.

About one-third of Bon Secours’ approximately 13,400 employees are 50 or older, and the health system’s HR team has been working diligently to retain as many of them as possible. About a decade ago, the organization’s leaders began allowing employees to work as few as 16 hours a week and still qualify for health coverage. Around the same time, leaders changed the pension eligibility requirements for the organization’s defined benefit plans so that employees who move to a part-time schedule won’t suffer financially. Pension payments were previously calculated based on an employee’s salary during his or her last five years of service. But under the new policy, payments are based on the five highest-earning years. Also gone are rules that forbade retirees from returning to work at the hospital for at least one year after their departure.

Within the past year, Bon Secours has worked with its benefits provider to increase staff at a call center that answers retirement questions from hospital employees. Robust succession planning is also key to minimizing disruptions. During evaluations, supervisors ask employees about their long-term career goals and who could fill their role should it become vacant. The conversations occur all over the hospital, regardless of an employee’s age or position. That uniform approach reduces the likelihood that the discussions can be construed as ageist, says Jim Godwin, vice president of human resources at the health system.

Many customer-centric companies also encourage older workers to stay on the job longer because they recognize that these individuals have often forged strong relationships with clients over the years, says Jason Russell, total rewards director at SAP North America, based in Newton Square, Pa.

That belief has prompted SAP to expand opportunities to keep older employees on the job, even on different terms, Russell says. This year, the company plans to introduce job sharing and a part-time work option. Last year, the technology company started a fellowship program to give experienced staff the opportunity to rotate across the organization and develop deep knowledge in certain areas to share with others, creating an in-house network of experts. “We want to give them an opportunity to still contribute,” Russell says. “You need to give people ways to adapt to their changing situations.”

Business leaders must adapt to their changing situations, too. That’s why supporting workers as they head to retirement is a smart way to secure a brighter future for everyone.

Theresa Agovino is a freelance writer based in New York City.

Related Articles

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.