Financial Wellness Could Be Key to Reducing Employee Turnover

Cutting back on these benefits could be short-sighted, SHRM research shows

LAS VEGAS—The COVID-19 pandemic brought new economic stresses for many employees. Then, as the economy recovered, employee turnover rates rose sharply.

These developments highlight the importance of helping to improve employees' financial well-being.

Although the pandemic caused some organizations to reduce spending on non-health-related benefits last year, financial wellness offerings—including access to emergency funds, financial planning, and tuition and student loan assistance—could receive renewed consideration to improve employee well-being, increase employee retention and attract new hires, according to a new survey report by SHRM and financial services firm Morgan Stanley.

Unlocking the Full Potential of Financial Wellness Benefits was released Sept. 11 at the SHRM Annual Conference & Expo 2021, taking place in Las Vegas and virtually.

To determine the current state of financial well-being in the U.S., as well as how employers are responding to this new imperative, in June 2021 SHRM and Morgan Stanley surveyed 1,000 working Americans, 1,000 unemployed Americans who lost or left their job since the start of the COVID-19 pandemic, and 1,205 HR professionals.

Meeting Employees' Needs

Nearly 3 in 4 (74 percent) HR professionals surveyed said their organization has not added new benefits or expanded existing benefits to help employees manage their financial stress since the start of the pandemic. At the same time, American workplaces are seeing record employee turnover, with more U.S. workers quitting their jobs than at any time in at least two decades.

Workers who believe their employers don't care about their well-being—physical, emotional and financial—often feel less engaged at work and are more likely to seek employment elsewhere. This may especially be true when they are experiencing anxiety about their financial situation.

A Range of Benefits

The most common financial wellness benefits offered by employers were:

- Retirement savings plans (offered by 95 percent of HR professionals' organizations)

- Safety net insurance, such as life and disability insurance (89 percent).

Fewer employers offer the following benefits:

- Financial planning for long-term security, such as sessions with a financial advisor on wealth management, investments and estate planning (35 percent).

- Financial coaching on the basics of personal finance, such as advice about personal budgeting, savings, debt and credit management (24 percent).

- Emergency savings funds (15 percent).

The surveyed HR professionals who offered these financial wellness benefits indicated that the offerings are being used more since the start of the pandemic, especially emergency funds (cited by 24 percent), financial planning (20 percent) and financial coaching (22 percent).

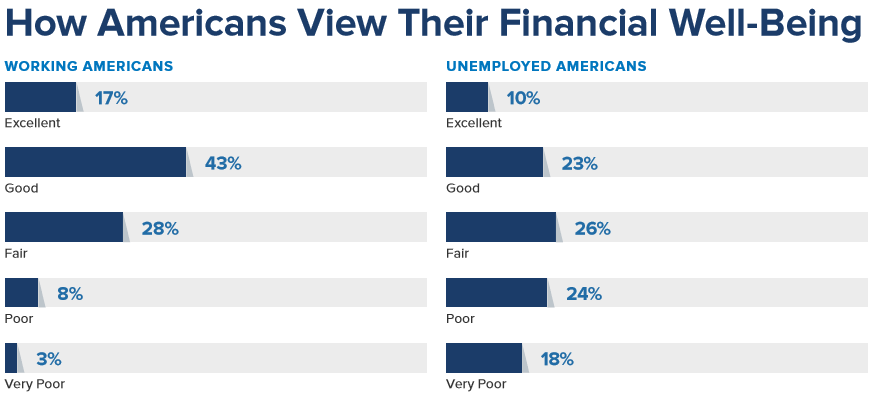

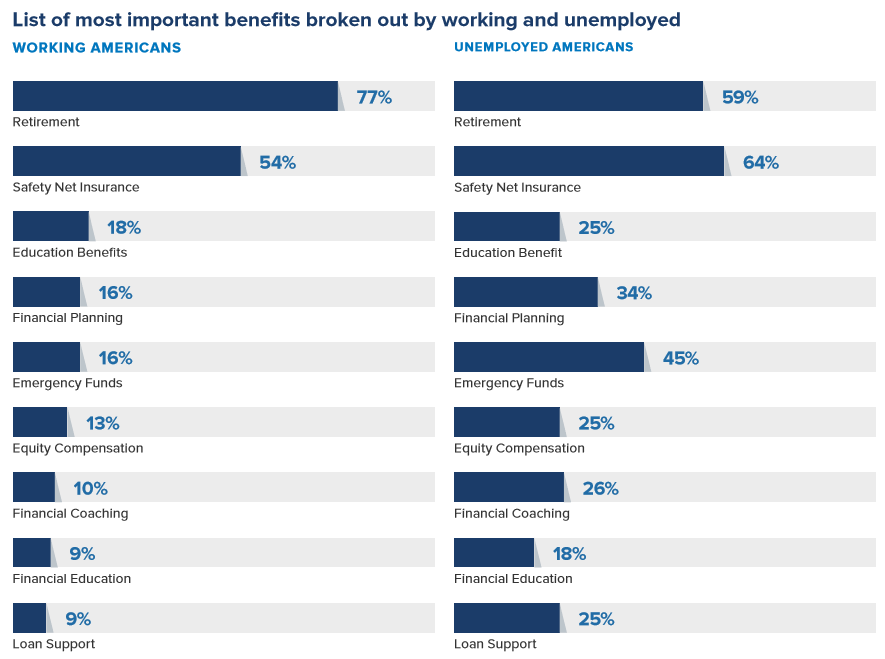

Employees' Differing Needs The existing workforce and the future workforce—which includes the currently unemployed—have different financial needs and values, so organizations that seek to retain current employees and hire from among the unemployed may need to adopt different strategies for these two groups. Source: Unlocking the Full Potential of Financial Wellness Benefits (September 2021). |

Education Benefits

Education benefits—such as tuition reimbursement, 529 plans, and employer-provided student loan repayment—are offerings that employees value highly: 18 percent of working Americans consider these one of the most important employer-sponsored financial wellness benefits for their financial needs and goals, the survey showed.

Just over 1 in 10 HR professionals (11 percent) say the use of education coverage has increased since the start of the COVID-19 pandemic, while 14 percent say their employer plans to focus on these benefits in the coming year.

Large organizations with 5,000 or more employees are more likely to offer education benefits (73 percent do so) than organizations with fewer than 500 employees (36 percent).

The Society for Human Resource Management supports expanding employer-provided education assistance to include student loan repayment and the monetary limit increased to give employers flexibility in the design of benefit offerings for recruitment and retention purposes.

"SHRM has long championed policies that allow employers to offer education assistance programs relevant to the modern workforce," said James Redstone, director of public policy at SHRM. "Greater certainty regarding the tax treatment of education assistance is an important step in expanding the availability of such benefits."

Emergency Funds vs. Retirement Savings

Although just 15 percent of surveyed HR professionals said their employer offered emergency funds—typically in the form of payroll advances or emergency savings funded through payroll deductions—45 percent of unemployed Americans, and 16 percent of working Americans, feel this is one of the most important employer-sponsored financial wellness benefits.

The much larger number of unemployed who value emergency funds seems to indicate this is a benefit that becomes more valued in the midst of job loss.

Of HR professionals whose organization offers emergency funds, nearly 1 in 4 (24 percent) indicated the use of emergency funds has increased since the start of the pandemic. However, just 6 percent of HR professionals said their employer plans to focus on emergency funds in the next year to address employee financial stress.

"Employer interest in emergency savings programs lies both in the direct potential benefit to workers, as well as a benefit to employers in the form of higher employee satisfaction," said Craig Copeland, senior research associate at the nonprofit Employee Benefit Research Institute. Addressing short-term savings needs "could lead to better long-term results, as emergency savings—distinct from retirement savings—could help preserve assets in [defined contribution retirement] plans that otherwise might be tapped for emergencies."

"Sometimes, the most effective solutions are the most basic," said Susan Shoemaker, a retirement advisor working in the Southfield, Mich., CAPTRUST office. "While it takes time, encouraging a participant to save enough to cover at least three months' expenses is the most practical approach to heading off an emergency."

Women at Higher Risk

Thirty-five percent of surveyed working women said their financial health or situation had suffered due to the pandemic, compared to 23 percent of working men.

Apart from the pandemic, the report cited factors contributing to the gender gap in financial well-being such as:

- Wage inequity. Women are disproportionately represented in lower-wage jobs, according to Pew Research Center.

- Family responsibilities. Women take more breaks from the workforce to care for family, Pew Research Center also noted.

- Life span. Women live longer and therefore must invest more into retirement, according to the National Center for Health Statistics.

"Even though it is significantly smaller than it once was, the gender pay gap remains and is having a significant impact on women's ability to save for retirement," the U.S. Government Accountability Office recently reported.

Retention Strategy

Employers can use financial wellness programs as part of an employee retention strategy, the report explains, by assessing the financial needs of the workforce and then taking steps to:

- Identify short-term goals such as engaging more employees in the program or researching other financial wellness programs.

- Identify long-term goals such as making changes to the current financial wellness program.

- Establish metrics to measure success such as utilization rates, program costs, employee retention, contributions to retirement plans, automatic savings programs and health saving accounts, as well as employee feedback regarding financial stress levels, debt levels, retirement readiness and financial literacy.

Employee Communications

Many employees have a limited understanding of the benefits available to them or how helpful these offerings can be to their financial health. SHRM's report advises employers to:

- Adopt a compelling communication strategy. In addition to one-on-one advice, seminars and online tools, effective communication is key to a successful financial wellness program. This can be achieved by creating a financial wellness logo or slogan, or an infographic pointing to research on the benefits of financial wellness programs.

- Use targeted communication. Certain segments of your workforce will value some benefits more than others. Differences in the way benefits are valued are common among men, women, executives, managers and line staff, for instance. Tailor your message to each group to show them how the benefits will help their unique situations.

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.