Small Employers Cut Health Care Costs Using Stand-Alone HRAs

Qualified small employer HRAs are a low-cost alternative to group coverage

Update: The IRS announced 2019 contribution limits for qualified small employer (QSE) health reimbursement arrangements (HRAs) in Revenue Procedure 2018-57 on Nov. 15, 2018. For tax years beginning in 2019, small businesses can offer QSEHRAs with funding of up to $5,150 for self-only employees ($429.17 per month) and $10,450 for employees with a family ($870.83 per month). The monthly limit reflects the annual limit over a period of 12 months. For employees who become eligible for the QSEHRA midyear, the limits must be prorated to reflect the total amount of time the employee is eligible. |

The qualified small employer HRA (QSEHRA), created by Congress in December 2016, is a way for small businesses with fewer than 50 full-time employees to offer nongroup health benefits. By using a stand-alone QSEHRA, small employers can offer their workers a tax-free monthly contribution to purchase their own health care policies, either through an insurance broker or on the Affordable Care Act (ACA) marketplace exchange.

If the premium is greater than the employer's monthly contribution, however, the employee pays the difference. If the contribution is more than the monthly premium, employees can use the extra funds to pay for out-of-pocket health costs, as they would do with a traditional HRA.

Employers with fewer than 50 full-time or equivalent employees are not subject to the ACA's employer mandate, which requires large employers to provide most full-time employees with ACA-compliant group coverage.

Another New HRA Proposed In October 2018, the Trump administration issued proposed regulations that would let employers, including those with 50 or more full-time employees, fund individual-market premium-reimbursement HRAs similar to QSEHRAs. One significant difference between QSEHRAs and the proposed HRAs, however, involves the availability of a premium-assistance tax credit/subsidy for coverage bought on an ACA marketplace exchange. Those using a QSEHRA to purchase an exchange policy may be eligible for a tax credit/subsidy, while those using a premium-reimbursement HRA apparently would not. See the SHRM Online article Regulations Aim to Let Employees Use HRAs to Buy Health Insurance. |

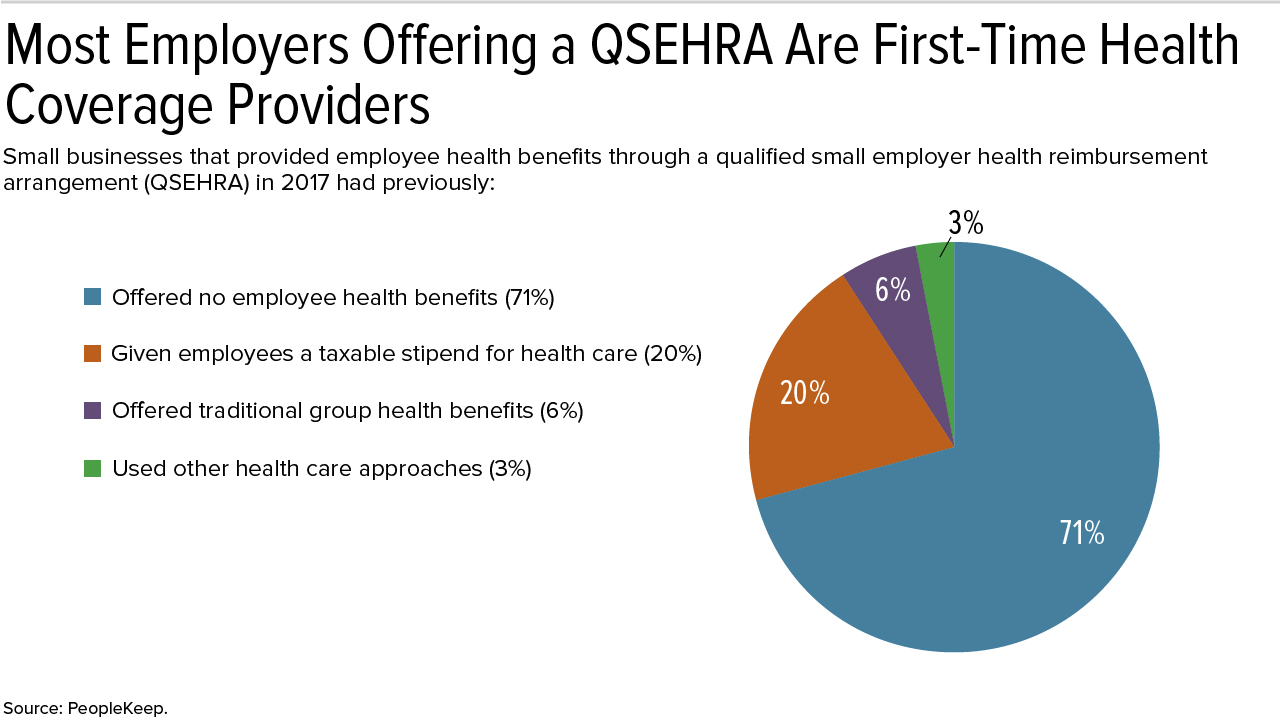

Lower Employer Costs

"There are many reasons small businesses choose to offer personalized health benefits like the QSEHRA, but one of the biggest reasons is cost," said Caitlin Bronson, a content specialist at Salt Lake City-based PeopleKeep, a benefits software company. "Thanks to rising costs and increasing government regulation, traditional group health benefits have become too expensive, too complex and too one-size-fits-all for most small businesses," she noted.

Bronson authored The QSEHRA: Annual Report 2018, which analyzed data from more than 600 small businesses and nearly 4,000 employees who were early adopters of the QSEHRA benefit last year.

Average monthly QSEHRA employer contribution amounts, the data showed, were:

- 38 percent smaller than the average small-employer contributions to group premium plans for single coverage.

- 47 percent smaller than average small-employer contributions to group premium plans for family coverage.

Small employers offering a QSEHRA in 2017 gave an average monthly contribution of:

- $280.20 per employee with self-only coverage.

- $476.56 per employee with family coverage.

In comparison, small businesses that offered group health insurance coverage spent an average $454.67 per employee per month for single coverage and an average $900.08 per employee per month for family coverage, according to the 2017 Employer Health Benefits Survey by the nonprofit Kaiser Family Foundation.

The IRS issues annual contribution limits for QSEHRAs, and last year nearly a quarter (22 percent) of participating employees received the 2017 maximum monthly contribution of $412.50 for self-only coverage or $833.33 for family coverage, PeopleKeep found.

For 2018, the monthly maximum QSEHRA limits are $420.83 for self-only and $854.16 for family coverage.

[SHRM members-only toolkit: Managing Health Care Costs]

Just Getting Started

According to the Society for Human Resource Management's 2018 Employee Benefits survey report, to be released in June, just 1.4 percent of responding HR professionals at organizations with fewer than 50 full-time employees or equivalents offered a QSEHRA.

"The percentage of small businesses offering a QSEHRA is still very small, given that it's only been around for a year and hasn't been well-publicized," Bronson said. "We estimate, however, that about 5,000 small businesses are offering a personalized health benefit of some kind—meaning benefits that involve tax-free company money being given to employees, who make their own health care purchases," such as through private health care exchanges. This approach is also called defined contribution health care.

Based on internal market research, "we believe the category of personalized health benefits will grow to about 1 million businesses by 2025," with QSEHRAs playing a significant role in that expansion, Bronson said.

An ERISA Question

The December 2016 bill that created QSEHRAs, the 21st Century Cures Act, amended the Employee Retirement Income Security Act (ERISA) to exclude QSEHRAs from ERISA's definition of a group health plan. However, the law did not specifically exclude QSEHRAs from the rest of ERISA.

"Small employers that plan to offer QSEHRAs should be cautious before presuming that ERISA would not apply to a reimbursement arrangement," said Danielle Capilla, senior vice president of compliance and operations at United Benefit Advisors, an alliance of independent benefit advisory firms.

Because QSEHRAs are new, the extent to which ERISA applies to them is still untested, she noted, so "a risk-averse small employer should treat a QSEHRA as an employee welfare benefit plan covered under ERISA and [should] comply with applicable ERISA requirements, such as having a written plan document and summary plan description, as well as following ERISA's fiduciary and other rules."

An employer seeking to establish a QSEHRA must notify its employees about "the effect that QSEHRA coverage might have on the employees' entitlement to a federal tax credit to purchase coverage through an [ACA] exchange," advised Ken Mason, a partner at law firm Spencer Fane in Overland Park, Kan. "Ordinarily, this notice must be provided at least 90 days before the beginning of the year for which the QSEHRA will be in effect."

Since the passage of the Cures Act, the Department of Labor issued guidance on QSEHRAs in a set of ACA compliance FAQs (December 2016), and the IRS addressed QSEHRA compliance in Notice 2017-20 (February 2017) and Notice 2017-67 (October 2017).

One point made in the most recent IRS notice: If an employer providing a QSEHRA benefit endorses a particular individual health insurance policy, form or issuer, "the coverage may constitute a group health plan" subject to ACA reporting and other requirements. However, providing employees with information about the ACA marketplace exchange or the ACA's premium tax credit "is not an endorsement of a particular policy, form, or issuer of health insurance."

Related SHRM Articles:

New Final Rule Lets Employees Use HRAs to Buy Health Insurance, SHRM Online, June 2019

Will Allowing HRAs for Plan Premiums Be a Game-Changer?, SHRM Online, June 2019

QSEHRAs Help Small Employers Solve the Health Care Coverage Puzzle, SHRM Online, May 2019

Health Care Consumerism: HSAs and HRAs, SHRM Online Benefits, updated March 2018

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.