114 Multiemployer Pension Plans Projected to Fail Within 20 Years

Failing union pensions may seek relief through reduced payouts

As many as 114 multiemployer pension plans covering nearly 1.3 million workers are severely underfunded and headed toward failure within the next 20 years.

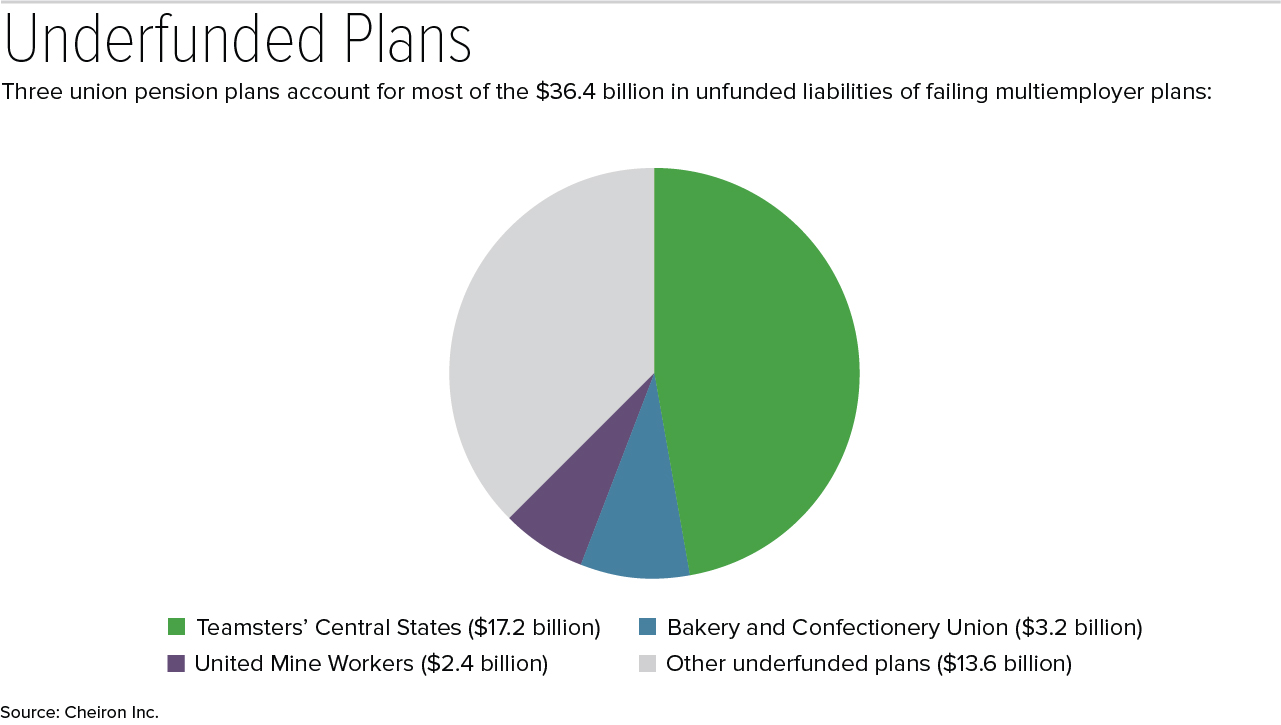

The forecast, from a new analysis by actuarial consulting firm Cheiron Inc., draws on the latest annual financial reports filed by multiemployer pension plans with regulators. The troubled plans have total assets of $43.5 billion and liabilities of $79.9 billion, leaving unfunded liabilities—future benefit payouts promised to retirees and beneficiaries for which reserve funds have not been set aside—of $36.4 billion.

Multiemployer pension plans, also known as Taft-Hartley plans, cover unionized workers and pensioners. Employer contributions are determined by collective bargaining, and the plan is governed by a joint labor-management board of trustees. Failing multiemployer plans must inform regulators that they are in "critical and declining" status, in keeping with the Multiemployer Pension Reform Act. The law requires pension plans to notify regulators annually if their financial condition is worsening and they expect to fail within 20 years.

"Traditionally, participants in healthy multiemployer pension plans have been forced to pay for the guaranteed benefits of retirees and their families in failed plans" through the Pension Benefit Guaranty Corp. (PBGC), the federal agency that guarantees participants a minimum pension even if their plans fail, said Joshua Davis, a principal consulting actuary at Cheiron's Portland, Ore., office. As more plans fail and premiums rise, "it will push other plans into insolvency with terrible consequences for communities across the country," he said.

The PBGC recently projected that it expects its insurance program for multiemployer pension plans will run out of money by the end of 2025. "As the demand for PBGC financial assistance for insolvent multiemployer plans increases, it will further strain PBGC's depleting assets—leading to estimated insolvency of the multiemployer insurance fund by the end of 2025," the PBGC reported. "If that happens, we won't have the money to pay PBGC guarantees at current levels to multiemployer plan participants when their plans run out of money."

Just three of the pension plans account for $22.8 billion—or more than 62.5 percent—of the $36.4 billion in unfunded liabilities of failing multiemployer plans, Cheiron found. The Teamsters' Central States, Southeast and Southwest Areas Pension Plan (usually shortened to "Teamsters' Central States") has the most unfunded liabilities at $17.2 billion, followed by the Bakery and Confectionary Union's plan ($3.2 billion) and the United Mine Workers' ($2.4 billion).

Multiemployer plans "pose a severe threat to the PBGC," said John Lowell, an Atlanta-based partner and actuary with October Three, a pension advisory firm. "The industries that historically have been the large players in the multiemployer space—teamsters and mining, for example—have been in decline in recent years. When retirees far outweigh the number of active participants, as in most declining industries, there is little hope of ever getting those plans well-funded without congressional intervention."

However, sponsors of single-employer plans shouldn't be overly concerned about a spillover threat to the PBGC's single-employer system, Lowell said. "The PBGC's own financial reports and projections indicate that its single-employer system is strong and sound," he noted.

[SHRM members-only toolkit: Designing and Administering Defined Contribution Retirement Plans

Green and Red Zones Most multiemployer pension plans continue to be in the green zone—meaning they are neither in critical nor endangered status as defined by the Pension Protection Act—according to a survey of the latest zone certifications by Segal Consulting, an HR advisory firm. The average funded percentage for these calendar-year plans is stable at 87 percent. However, "the survey finding that about two-thirds of calendar-year plans are in the green zone should not obscure the fact that just about half of all participants in the survey are in red-zone plans," the Segal survey report states. "Significantly, about one-quarter of the participants in the survey are in plans that are also in 'critical and declining' status." |

Reducing Plan Payouts

The Multiemployer Pension Reform Act, passed at the end of 2014, allows severely distressed multiemployer plans to seek permission from the U.S. Treasury Department to reduce future payouts to avoid bankruptcy and termination, and by doing so to keep solvent the PBGC's multiemployer pension insurance fund.

A Treasury Department webpage provides a list to multiemployer pension plans that have applied to reduce future payouts.

An attempt by the Teamsters' Central States plan to reduce future payouts last year was denied by the Treasury Department, which cited flaws in the application and claimed that the proposed reductions would not make the plan solvent.

Last December, however, the Treasury for the first time approved an application from a troubled multiemployer pension plan—the Iron Workers Local 17 Pension Fund in Cleveland—to reduce vested benefits. On Aug. 3, trustees of the New York State Teamsters' Conference Pension and Retirement Fund were notified that their application to reduce pension benefits was accepted.

The Treasury's approval of these benefit reductions, as well as the rejections given to other plans—including Teamsters' Central States—"provides a road map for a successful application," Lowell said. "I would expect to see more applications, with a high percentage crafted in such ways as to be approved."

As to whether the trustees of the Central States plan might again seek the Treasury's consent to reduce payouts, "I suspect that the trustees are at least evaluating their options," Lowell said. "They know that to sustain the plan they will need to take some action, with an application to reduce benefits being the most plausible. The question is whether such a proposal can be crafted that makes sustainability of the plan likely."

Related SHRM Articles:

Treasury: Iron Workers' Troubled Multiemployer Pension May Reduce Payouts, SHRM Online, December 2016

Lessons from the Central States Pension Fund 'Rescue Plan' Denial, SHRM Online, July 2016

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.