A 401(k) Twist on Student-Loan Aid

A new benefit keeps student debt from derailing retirement savings

Update: IRS Releases Private Letter Ruling On Aug. 17, 2018, the IRS made public Private Letter Ruling 201833012, responding to an employer that proposed amending its 401(k) plan to offer a student loan benefit program under which it would make an employer nonelective contribution on behalf of an employee, conditioned on that employee making student loan repayments. The IRS responded, in part, that the "proposal to amend the plan to provide [student loan repayment] nonelective contributions under the program will not violate the 'contingent benefit' prohibition of section 401(k)(4)(A) and section 1.401(k)-1(e)(6)." For more about the ruling and its expected effect on this type of benefit program, see the SHRM Online article IRS Allows 401(k) Match for Student Loan Repayments.

|

Abbott Laboratories recently launched a benefit that helps employees save for retirement while paying off student loans. The benefit also sidesteps the taxes that direct student-loan repaymentassistance would trigger. Other employers may be inspired to follow Abbott's lead, but there are some factors they should consider.

Here's how the new Freedom 2 Save program works at Abbott, a research and development company headquartered in Lake Bluff, Ill. Full- and part-time employees who qualify for the company's 401(k) and are also contributing 2 percent of their eligible pay toward their student loans through payroll deductions receive an amount equivalent to the company's traditional 5 percent 401(k) match, deposited to their 401(k) accounts. The twist is that program recipients will receive the match without being required to make any 401(k) contributions of their own, allowing them to use more of their earnings to pay off student debt.

"The benefit responds to recent financial challenges facing young employees—many of whom have undergraduate and advanced degrees in science, engineering and business fields—and adds to the strong appeal of joining the Abbott family," the company stated in a news release.

"We see our young professionals coming to us with a problem: Student loan debt payments keep them from setting aside the money they'd like to put in savings for retirement," said Steve Fussell, executive vice president for human resources at Abbott. "Helping them with this challenge is the right thing to do."

Abbott isn't the first employer to offer this "twist"; in 2016 Prudential Retirement, a provider of 401(k) plan administration services, launched a similar benefit. Its adoption by a high-profile employer outside of the financial services community, however, signals that this approach may be going mainstream.

A Challenge for Young Workers

Federal statistics show that a typical 2017 college graduate owes about $39,400 in student loans, and borrowers ages 20 to 30 are making average payments of $351 a month to service their loans. Those payments often leave nothing to invest in an employer's retirement plan, which may explain why about 66 percent of Millennials don't have anything saved for retirement, with many resigned to working longer to help make up the gap.

With every decade that new graduates wait to start saving for retirement, the amount they need to save roughly doubles, Fussell noted.

[SHRM members-only toolkit: Designing and Managing Educational Assistance Programs]

Meeting a Need

Abbott hired more than 1,000 people under age 35 last year in the U.S., Fussell said. More than a third of those ages 31 to 35 had a master's degree, and another third had a doctorate degree, meaning they're likely to carry more debt than a typical undergraduate hire.

One of those hires is Rariety Monford, 26, an engineer in the company's professional development program who said she plans to take advantage of the new benefit.

"I was out of state for my biomedical engineering degree, so my student loans are well more than the average," Monford said. "Paying it off is my No. 1 goal. Abbott also has a tuition-assistance program that I intend to use when I start graduate school in the fall, but the Freedom 2 Save program will be a huge help in making sure I'm saving for the future while still aggressively paying off my loans."

If new hires with student debt join Abbott at a starting annual pay of $70,000 and take advantage of the program, they could see $54,000 accumulate in their 401(k) account over a 10-year period, assuming a 6 percent average annual return and yearly merit pay increases of 3 percent—without any 401(k) contribution of their own, Fussell said. "That amount could be worth hundreds of thousands of dollars in additional retirement savings by age 60," he noted.

A Tax Break, Too

Abbott's approach avoids the taxes triggered when an employer directly gives employees funds to help pay off their student loans.

"If the employer simply pays a portion of the employee's student-loan debt, that results in taxable W-2 wages to the employee," said attorney Elizabeth Thomas Dold, a principal with Groom Law Group in Washington, D.C. "Conversely, if the employer makes a contribution to a tax-qualified retirement plan to encourage participants to repay these debts, there is generally no taxation until retirement" on employer contributions, subject to annual IRS limits.

Dold cautioned, however, that "depending on the structure of a particular arrangement, a number of [IRS compliance] issues could arise" over the program's design and how such "matches" are earned, and targeting extra contributions to employees who are repaying student debt might affect annually required 401(k) nondiscrimination testing that ensures 401(k) plans are equitable to employees. It also would be necessary to amend the retirement plan document, she said.

"The benefits community eagerly awaits additional guidance in this area from the IRS," Dold added.

"If a firm can afford it, a good solution is combining debt forgiveness and a 529 plan so that those with families can save for their children's or grandchildren's educations" on a tax-advantaged basis, said Bill Gimbel, president of LaSalle Benefits, a tech-enabled insurance brokerage firm in Northbrook, Ill. With a 529 plan, contributed funds grow tax free and can be withdrawn tax free for educational purposes.

A Legislative Fix

While Abbott's program is an innovative workaround that avoids taxes levied on direct student-loan repayment contributions, the Society for Human Resource Management (SHRM) would like Congress to make employers' loan-repayment aid a tax-free benefit treated the same as tuition assistance under Section 127 of the Internal Revenue Code.

For 2018, Section 127 lets employees exclude from taxable income up to $5,250 per year in employer-provided educational assistance for undergraduate or graduate studies or certificate work. The benefit covers tuition, fees, books, supplies and equipment.

SHRM supports two bipartisan bills to expand Section 127: the Employer Participation in Student Loan Assistance Act would make employer-provided student-loan repayment contributions tax free within annual limits, and the Upward Mobility Enhancement Act would increase allowable tax-free tuition assistance to $11,500 per calendar year.

Cost Hurdle Remains

Only big employers may have the resources to offer student-debt repayment benefits, either directly or through an "out of the box" approach such as Abbott's, said LaSalle Benefits' Gimbel. "Smaller and midsize companies just don't have the finances to offer something of this caliber," he said.

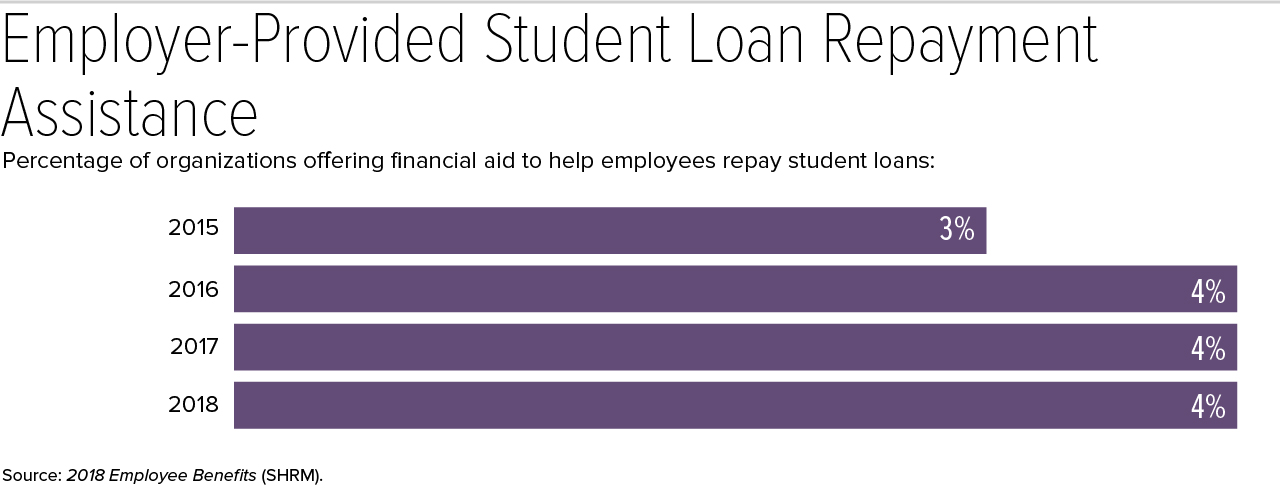

SHRM's 2018 Employee Benefits Survey, which polled SHRM members at organizations of all sizes earlier this year, found that student loan repayment was offered by just 4 percent of organizations, a figure unchanged since 2016 (SHRM first began surveying members about the issue in 2015).

Employers appear cautious about adding a new and potentially expensive financial benefit, even if it is highly valued by job candidates carrying student debt.

Related SHRM Article:

Welcome, Generation Z: Here’s Your Benefits Package, SHRM Online Benefits, July 2018

Tips for Launching a Student-Loan Repayment Benefit, SHRM Online Benefits, October 2017

Student Loan Assistance Benefits See Little Growth, but Need Is Real, SHRM Online Benefits, June 2017

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.