IRS Allows Midyear Enrollment and Election Changes for Health Plans and FSAs

SHRM sought flexibility as pandemic alters employees' needs

updated Jan. 4, 2021

Update: Appropriations Act Extends FSA Relief The Consolidated Appropriations Act that President Trump signed at the end of 2020 allows employers that sponsor health or dependent care flexible spending accounts (FSAs) to permit participants to roll over all unused amounts in these accounts from 2020 to 2021 and from 2021 to 2022. Employers may also allow employees to prospectively change their health or dependent care FSA contribution rates during 2021 without experiencing a permitted election-change event. Employers wishing to offer optional FSA relief provisions must amend their Section 125 cafeteria plan to incorporate the changes. The amendment may be retroactive as along as it is adopted no later than the last day of the calendar year following the year in which the amendment is effective. See the SHRM Online articles: |

The article below was last updated on June 10, 2020

- Notice 2020-29 provides increased flexibility for participants to make midyear health plan, health FSA and dependent care FSA election changes.

- Notice 2020-33 increases the carryover limit permitted for health FSAs.

These changes, which apply only to plan year 2020, had been advocated by the Society for Human Resource Management (SHRM). The new guidance is permissive; employers are not required to make these plan changes.

Health Plan Enrollments and Elections

In IRS Notice 2020-29, the agency said it would allow increased flexibility regarding midyear election changes for group health plans and FSAs. Employers, at their discretion, may allow employees to make either or both of these changes:

- Enroll in employer-sponsored health plans during the plan year by making a new election. Employees may do so even if they had previously declined enrollment.

- Switch health plans or tiers within plans. Employees will be able to drop current coverage to enroll in different coverage offered by the same employer or change from single coverage to family coverage, for instance.

"The IRS notice says that employers are not required to provide unlimited changes and the employer can set a timeframe to make changes," said Chatrane Birbal, vice president, public policy, at SHRM.

Although allowing employees to make these newly permitted plan changes during 2020 is optional for employers, many "will want to enable employees to enroll or revoke an enrollment election in various group health plan options," noted Gary Kushner, president and CEO of HR and benefits consulting firm Kushner & Company in Portage, Mich.

Difficult Times

While under existing Section 125 cafeteria plan rules a change in the employment status of a spouse would be a life event that allows a midyear election change, the new guidance does not require that employees provide documentation of this, or that a requested election change be consistent with any change-in-status event.

Julie Stone, North America co-leader for the health management practice at HR consultancy Willis Towers Watson, noted that "from an enrollment/plan election perspective, I expect there are many people where both partners/spouses were employed and opted to be covered under one plan potentially with children. If that parent loses employment, the cost of family COBRA is likely to be much more costly than changing to the working spouse/parent's employer sponsored plan."

She added, "Given the unemployment and furlough rates, I think this is one of the most important aspects of the new guidance."

David Speier, managing director for benefits accounts at Willis Towers Watson, said that allowing midyear plan elections could mean that employees will "switch to a plan that increases the employer's financial burden during a difficult time," for instance if employees opt for a low-deductible plan with higher premiums paid by the employer, or shift from single coverage to a more expensive family plan. However, other midyear changes could reduce an employer's cost sharing, "as when employees elected a dental plan but now opt out because they can't use it this year," Speier added.

FSA Enrollments and Elections

For both health FSAs and dependent care FSAs (used to fund caregiving expenses with pretax dollars), employers can let employees enroll, drop coverage, and increase (within the annual limit) or decrease payroll-deducted contributions during 2020.

"This is welcome relief, and many employers will consider providing it under their plans," said William Sweetnam, legislative and technical director at the Employers Council on Flexible Compensation, which represents sponsors of account-based benefit plans.

Stone explained, "At a time where some people may be cash-strapped, deferring elective procedures, new eyeglasses, etc., may well make sense, and so being able to suspend contributions to a health FSA or limited purpose dental/vision FSA is important."

Kushner blogged, "Many employers would embrace enabling dependent care FSA participants to increase (or more likely decrease or revoke) their elections if schools and day care centers are closed, or if the employee is working from home."

However, for any FSA, "employers may be more reluctant to enable employees to decrease or revoke their election if they've already claimed their previous full election amount and payments have been disbursed," he added.

In 2020, employees can contribute $2,750 to a health FSA, including to a limited-purpose FSA restricted to dental and vision care services, which can be used in tandem with a health savings account (HSA).

The dependent care FSA maximum, which is set by statute and not adjusted annually for inflation, is $5,000 a year for individuals or married couples filing jointly, or $2,500 for a married person filing separately, subject to earned income limits.

[SHRM members-only forms: COVID-19 Midyear Election Change Attestation]

FSA Use-It-or-Lose-It Rules

Existing IRS rules provide an employer two options for unused health care FSA funds: A grace period into the new year during which employees can continue to spend FSA funds from the previous year, and the ability to carryover over a limited amount of funds from the previous year. Employers can choose to incorporate either the grace period or the carryover feature, or neither, but not both.

The new guidance changes the rules for both these provisions for plan year 2020.

Grace Period Extension

IRS rules allow employers to add a two-and-one-half-month grace period immediately following the end of each FSA plan year, during which health FSA holders could spend any funds remaining in the account. For calendar year health FSAs, the grace period ends March 15. The new guidance will extend the grace period to the end of 2020.

For plan years ending before Dec. 31, 2020, employers can amend a health or dependent care FSA plan to permit participants to "spend down" through year-end 2020 any remaining amounts from 2019 that would otherwise be forfeited. Employers can allow claims incurred at any time in 2020 to be applied to any remaining 2019 FSA balances.

Plan amendments that extend the claims period for health and dependent care FSAs may be effective retroactively to Jan. 1, 2020. All eligible employees should be informed of the changes.

Increased Carryover Cap

IRS Notice 2020-33, also released May 12, increases the amount of funds that health FSA participants can carry over without penalty at the end of the year for plans that use the carryover option. The carryover amount will now be indexed for inflation by making it 20 percent of the allowable payroll-deductible contribution limit, which is $2,750 for plan year 2020.

As a result, the maximum unused amount from a plan year starting in 2020 allowed to be carried over to the immediately following plan year beginning in 2021 is $550, up from the previous limit of $500.

[SHRM members-only HR Q&As: What options does an employer have with unused FSA funds?]

While Sweetnam called the inflation adjustment helpful, he noted that many have advocated allowing much larger carryover amounts or eliminating the use-it-or-lose-it rule completely. "I think that the limited amount of the increase means that the IRS and Treasury Department were concerned that they did not have the authority under the Internal Revenue Code to provide for a larger carryover amount," he suggested.

Notice 2020-33 also clarified that the previously provided temporary relief for high-deductible health plans (permitting them to cover COVID-19 related services at no cost) may be applied retroactively to Jan. 1, 2020.

Different Plans Had Different Rules Some midyear elective-contribution changes have long been permitted. For instance, changes to payroll deductions to fund 401(k) or similar defined contribution retirement plans, HSAs, and commuter benefit plans can be made at any time for any reason, although employers may limit changes for administrative purposes, such as to once per month. For employer-sponsored group health, dental and vision plans, however, changes are restricted. Under tax code Section 125, elective contributions typically can be changed only within 30 days of a qualifying event as determined by the IRS, such as marriage, divorce, job change, birth or adoption of a child, or when a dependent child reaches age 26. The new guidance carves out an exception for changes made during 2020 due to the COVID-19 pandemic. |

HSA-Eligibility Issues

Sweetnam noted an issue with the new guidance that could complicate matters for employees who had a 2019 health FSA and were newly enrolled in an HSA in 2020: An employer that carries over unused funds from a prior year to a current year under a general-purpose health FSA will not be eligible for HSA contributions for the entire current plan year.

"Carryover 2019 FSA amounts can be used to pay for health care expenses below the deductible in 2020, thus making participants [with both carryover health FSAs and new HSAs] ineligible to make HSA contributions in 2020," Sweetnam said. "Consequently, employers may want to consider the impact on HSAs as they decide whether to extend the claims period for health FSAs."

To avoid this issue, employers can allow 2019 carryover health FSA funds to be transferred an HSA-compatible, limited-purpose FSA, which can be used only for vision care and dental expenses.

SHRM Advocacy

"As employers and their employees navigate the current crisis, workplace health care has emerged as a critical issue requiring flexibility," Emily M. Dickens, SHRM corporate secretary, chief of staff and head of government affairs, wrote in an April 16 letter to IRS Commissioner Charles Rettig.

SHRM advocated flexibility on rollover provisions, time frames for claims, and midyear election changes to FSAs due to employees' evolving health care and child care needs as a result of COVID-19.

SHRM also requested a one-time, pandemic-related window for employees who may have declined coverage at the start of the calendar year to enroll in an employer's health plan, as the IRS is now allowing for 2020. "Many employers are struggling with employee requests for election changes and whether such a change would be permitted under IRS guidance," Dickens wrote.

In addition, SHRM asked the IRS to increase the annual $500 carryover limit for health FSAs for plans that use the carryover option.

"Many employees … carefully contemplated a health care FSA election based on [elective] medical procedures that will no longer occur," Dickens pointed out, and these employees should not be penalized because their anticipated annual medical expense estimates need to be adjusted.

Update:

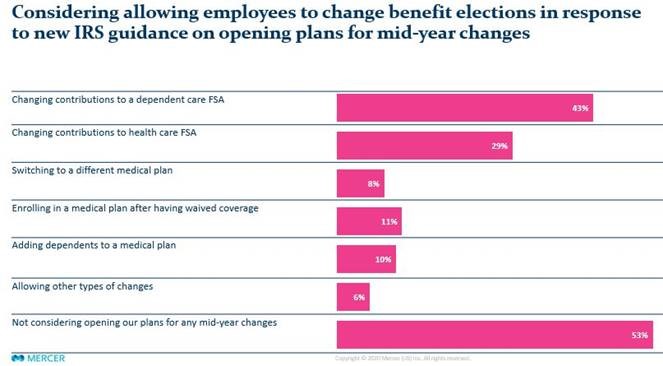

HR consultancy Mercer's COVID-19 survey, with responses through June 9 from nearly 300 large U.S. employers, asked if they would "reopen" their health plans and FSAs for the 2020 plan year to employees and their dependents, whether they currently participate or not, to make any type of midyear changes allowed by the IRS guidance.

Just under half (47 percent) of the employers surveyed indicated they will allow some type of mid-year change, with the most popular being changing contributions to a dependent care FSA (43 percent) and changing contributions to health care FSA (29 percent).

Fewer employers are planning to allow changes to medical plan elections, such as enrolling in a plan after having waived coverage or adding a dependent. Nevertheless, approximately 1 in 10 say they will allow these types of changes.

Source: Mercer COVID-19 survey, U.S. results as of 6/9/2020 (279 respondents, more than one response allowed).

"Allowing participants to change their contributions to dependent care or health FSAs can be a relatively simple way for employers to support employees coping with COVID-19 related issues," said Jay Savan, a partner in Mercer's health business. "Maybe a child's summer camp is closed, or someone cancelled some planned dental work, or a spouse is out of work and the employee just needs more money in their paycheck."

Savan said while there is very little downside in allowing dependent care FSA changes, employers should be mindful that there are some potential risks associated with allowing changes to health FSAs. These risks include immediate employee access to full account limits during a time when employers are hyper-focused on conserving cash, as well as the potential for employees to accelerate their use of health FSA funds and leave the plan in a deficit if they discontinue employment.

"Permitting enrollment changes midyear in core medical plans, however, brings with it much greater risk to the sponsor, such as incurring high cost claims and generally enabling adverse selection," Savan noted. "It can also have collateral impact on stop-loss reinsurance and other related contracts."

He advised employers to weigh these risks before liberalizing the terms of midyear enrollment in medical plans in 2020.

Related SHRM Articles:

Appropriations Act Permits Midyear FSA Elections, Unlimited Carry-over Amounts Through 2021, SHRM Online, January 2021

SHRM Asks IRS for Relief with Health Plan Compliance During Pandemic, SHRM Online, April 2020

Special COVID-19 Health Insurance Enrollment Windows and Waivers, SHRM Online, March 2020

2020 FSA Contribution Cap Rises to $2,750, SHRM Online, November 2019

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.