IRS Announces 2021 Limits for HSAs and High-Deductible Health Plans

Employers and employees contributed more to their HSAs last year

Updates: On May 10, 2021, the IRS announced health savings account (HSA) contribution limits for 2022. See the SHRM Online article IRS Announces 2022 Limits for HSAs and High-Deductible Health Plans. On April 29, 2022, the IRS announced HSA contribution limits for 2023. See the SHRM Online article IRS Announces Spike in 2023 Limits for HSAs and High-Deductible Health Plans. |

Health savings account (HSA) contribution limits for 2021 are going up $50 for self-only coverage and $100 for family coverage, the IRS announced May 21, 2020, giving employers that sponsor high-deductible health plans (HDHPs) plenty of time to prepare for open enrollment season later this year.

The annual limit on HSA contributions will be $3,600 for self-only and $7,200 for family coverage. That's about a 1.5 percent increase from this year.

In Revenue Procedure 2020-32, the IRS confirmed HSA contribution limits effective for calendar year 2021, along with minimum deductible and maximum out-of-pocket expenses for the HDHPs with which HSAs are paired.

| Contribution and Out-of-Pocket Limits for Health Savings Accounts and High-Deductible Health Plans | |||

|---|---|---|---|

| 2021 | 2020 | Change | |

| HSA contribution limit (employer + employee) | Self-only: $3,600 Family: $7,200 | Self-only: $3,550 Family: $7,100 | Self-only: +$50 Family: +$100 |

| HSA catch-up contributions (age 55 or older) | $1,000 | $1,000 | No change |

| HDHP minimum deductibles | Self-only: $1,400 Family: $2,800 | Self-only: $1,400 Family: $2,800 | No change No change |

| HDHP maximum out-of-pocket amounts (deductibles, co-payments and other amounts, but not premiums) | Self-only: $7,000 Family: $14,000 | Self-only: $6,900 Family: $13,800 | Self-only: +$100 Family: +$200 |

| Source: IRS, Revenue Procedure 2020-32. | |||

"The IRS contribution-limit increases are in line and similar to prior year increases, despite the COVID-19 environment," said Harrison Stone, general counsel at HSA services firm ConnectYourCare. "While some may view the increases as modest, every dollar matters right now for consumers when it comes to saving," he added.

"Plan sponsors should update payroll and plan administration systems for the 2021 cost-of-living adjustments and should incorporate the new limits in relevant participant communications, such as open enrollment and communication materials, plan documents, and summary plan descriptions," advised Jacob Mattinson and Judith Wethall, partners in the Chicago office of law firm McDermott Will & Emery.

"Employers should consider these limits when planning for the [upcoming] benefit plan year and review plan communications to ensure that the appropriate limits are reflected," advised Damian A. Myers, senior counsel at law firm Proskauer in Washington, D.C.

In the meantime, those enrolled in an HSA last year can top off contributions for 2019 through the COVID-19-related extended tax day deadline of July 15, 2020.

[SHRM members-only HR Q&A: Are employer contributions to an employee's health savings account (HSA) considered taxable income to the employee?]

Adjustments Reflect Inflation

Contribution limits for various tax-advantaged accounts for the following year are usually announced in October, "except for HSAs, which come out in the latter part of April or May," explained Harry Sit, CEBS, who writes The Finance Buff blog. The contribution limits are adjusted for inflation (rounded to the nearest $50) annually, using the Consumer Price Index for All Urban Consumers for the 12-month period ending on March 31. The catch-up contribution amount, however, is fixed by statute.

While increases in HSA contribution limits are tied to inflation rates, "health care costs continue to outpace inflation, which means Americans will spend more out-of-pocket each year," said Shobin Uralil, co-founder and chief operating office of Lively, an HSA services firm.

Nevertheless, "these new contribution limits will help increase the value of HSAs to individuals and families," Uralil said. "We're seeing growth in HSAs as a vehicle not only for health savings in the near term, but for anticipated health costs in retirement as well."

"While the increases are modest, they are an additional opportunity for Americans to prepare and pay for their health care needs," noted Stone. "Annual contribution-limit increases allow HSAs to maintain their value and further grow their role as a key retirement-planning building block."

Employer HSA contributions are not treated as taxable income but do count toward employees' annual contribution limit, Stone noted.

"Employers may make one up-front lump sum contribution, semiannual contributions, quarterly contributions, monthly contributions, per-pay period contributions, or any other regular interval in between," according to ABD Insurance & Financial Services in San Mateo, Calif. "The employer has full discretion in designing its HSA contribution strategy."

CARES Act Expands HSA-Eligible Purchases As part of the Coronavirus Aid, Response and Economic Security (CARES) Act signed into law at the end of March, account holders can now use HSAs, health reimbursement arrangements (HRAs) or health flexible spending account (FSAs) to pay for over-the-counter medications without a prescription. The coronavirus-related legislation also allows HSAs, HRAs and FSAs to pay for certain menstrual care products, such as tampons and pads, as eligible medical expenses. These are permanent changes and apply retroactively to purchases beginning Jan. 1, 2020. Being able to use an HSA to pay for over-the-counter medications "empowers individuals to better manage their own health care needs and reduces the administrative load on doctors' offices facing a strain on resources," said Alison Moore, vice president of marketing at HealthSavings Administrators, a firm that manages consumer-directed health accounts. In addition, the CARES Act allows HDHPs to cover telemedicine free of cost sharing through year-end 2021. A new safe harbor permits HDHPs to cover telehealth and other remote care services before participants have met their deductible without affecting their eligibility to make HSA contributions. These provisions are temporary and will sunset Dec. 31, 2021, unless Congress extends them or makes them permanent. "Altering the rules to include telehealth during the COVID-19 crisis will help to ease the burden on in-person facilities and help limit the spread of the virus by allowing people to receive care remotely without exposing themselves unnecessarily," said Chatrane Birbal, director of policy engagement at the Society for Human Resource Management. |

Contributions Were Up

Employers and employees contributed more on average to employees' HSAs last year, according HSA investment advisory firm Devenir's 2019 Year-End HSA Market Survey.

In January 2020, Devenir collected customer data on the previous year from the top 100 HSA plan administrators in the U.S., which are primarily banks and financial services firms. Among the findings:

- The average employer contribution in 2019 was $880 (among employers that made contributions), up from $839 in 2018 and $604 in 2017.

- The average employee contribution in 2019 was $2,034 (among employees who made contributions), up from $1,872 in 2018 and $1,921 in 2017.

Looking at employer contributions from a different angle, a March 2020 medical trends report from DirectPath, a benefits education, enrollment and health care transparency firm, and Gartner, a research and advisory firm, pegged average employer HSA contributions at the start of 2020 as follows:

- Single coverage HSA: $512

- Employee plus spouse: $996

- Family coverage HSA: $1,047

The findings are based on an analysis of more than 1,000 employer health plans in the firms' health plan benchmarking database.

More organizations are providing opportunities for employees to "earn" employer HSA contributions by participating in wellness activities, the firms noted, although employers should keep in mind that there will always be employees who will not participate in these programs.

"The key now is to educate employees on the value [of their HSAs] so they can best utilize them—and ultimately drive down health care costs for themselves and for their employers," said Kim Buckey, vice president of client services at DirectPath.

HSA participants who are able to do so should consider contributing up to annual limits "not only to take advantage of the tax savings, but also to ensure that they are putting themselves in a position to better afford their future health care," Uralil said. "Employers can do their part by extending HSA contributions as a benefit to their employees."

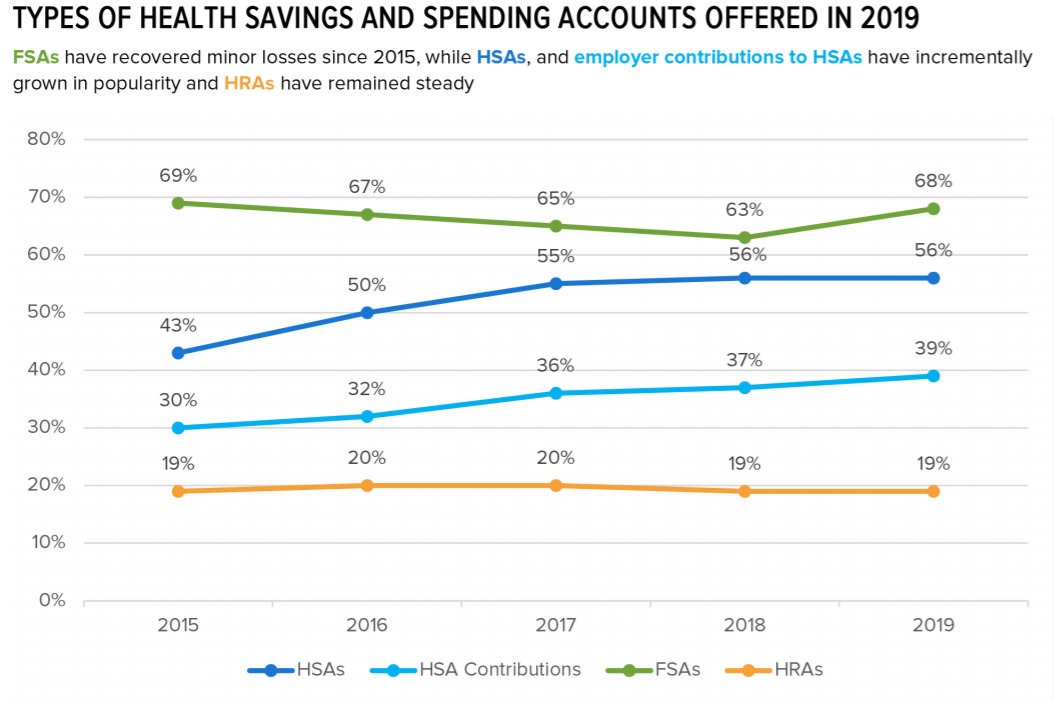

HSA Growth Outpaces Other Accounts The Society for Human Resource Management (SHRM) 2019 Health Care and Health Services report, with data from the 2019 SHRM Employee Benefits survey of 2,763 HR specialists, looked at the growth of workplace HSAs—and employer contributions to them—in comparison with FSAs and HRAs.

|

ACA's Limits Differ

There are two sets of limits on out-of-pocket expenses for health plans, determined annually by federal agencies, which can be a source of confusion for plan administrators.

The Department of Health and Human Services (HHS) establishes annual out-of-pocket or cost-sharing limits under the ACA for essential health benefits covered under an ACA-compliant plan, excluding grandfathered plans.

The HHS's annual out-of-pocket limits are higher than those set by the IRS, but to qualify as an HSA-compatible HDHP, a plan must not exceed the IRS's lower out-of-pocket maximums.

On May 14, HHS published the Notice of Benefit and Payment Parameters final rule for 2021 and posted a fact sheet that summarizes its most significant changes.

Below is a comparison of the two sets of limits:

| 2021 | 2020 |

Out-of-pocket limits for ACA-compliant plans (HHS) | Self-only: $8,550 Family: $17,100 | Self-only: $8,150 Family: $16,300 |

|

Family: $14,000 |

Family: $13,800 |

Related SHRM Articles:

401(k) Contributions 'Crowded Out' by HSAs—Does It Matter?, SHRM Online, February 2021

Employees Still Perplexed by HSA Plans During Open Enrollment, SHRM Online, November 2020

2021 FSA Contribution Cap Stays at $2,750, Other Limits Tick Up, SHRM Online, October 2020

IRS Raises 2021 Employer Health Plan Affordability Threshold to 9.83% of Pay, SHRM Online, July 2020

HHS 2021 Health Plan 'Parameters' Raise Out-of-Pocket Maximums, SHRM Online, May 2020

Related SHRM Resources:

2021 Benefit Plan Limits & Thresholds Chart

Open Enrollment Guide & Resources (2021 Inflation-Adjusted Limits & Thresholds)

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.