Open Enrollment: Voluntary Benefits Emphasize Choice

However, too much employer involvement can trigger ERISA compliance

This is the fifth in a series of articles on meeting open enrollment challenges. This article examines how employee-paid voluntary benefits can help to meet employees' needs.

updated on Nov. 8, 2017

Voluntary benefits can range from supplemental critical illness coverage to pet insurance or even auto and home insurance. Typically, these plans have group-rate premiums negotiated by the employer but paid by employees. In some cases, especially for health benefits, premiums are payroll-deducted on a pretax basis.

"Voluntary benefits can help to address possible financial gaps for employees," said Peter Marcia, the CEO of YouDecide, a voluntary benefits outsourcing firm based in Duluth, Ga. "When offering voluntary benefits, it's critical that the employer communicates how these benefits strategically complement the core offerings. An example of this is supplementing core medical plans with products to reduce potential out-of-pocket costs."

While employees typically pay for these premiums, they do so at group rates, "which most of the time is going to make the price lower than if the same coverage was purchased on an individual basis," said Kim Buckey, vice president of compliance communications at Birmingham, Ala.-based DirectPath, an employee engagement and health care compliance firm.

What's Trending?

As companies are gearing up for open enrollment, "we're seeing a bigger focus on voluntary benefits that might offset some of the new high-deductible health plans [HDHPs] that employers are rolling out," said Andy Edeburn, director of customer insight at Jellyvision, an employee communication software provider based in Chicago. "Specifically, employers are increasing their messaging around critical illness, accident, hospital indemnity and similar voluntary plans that can offset out-of-pocket costs under a high-deductible plan and offer a safety net."

Consider critical illness or hospital indemnity plans that reimburse the employee for specific medical treatments on a first-dollar basis, below the primary health plan's deductible threshold.

For some HDHPs, deductibles could be $2,000 to $5,000, or even higher. "If employees have purchased supplemental coverage, they could end up ahead of the game—or at least in a better place than they would have otherwise been, should they incur several thousand dollars in expenses below the [primary plan's] deductible threshold," Buckey explained.

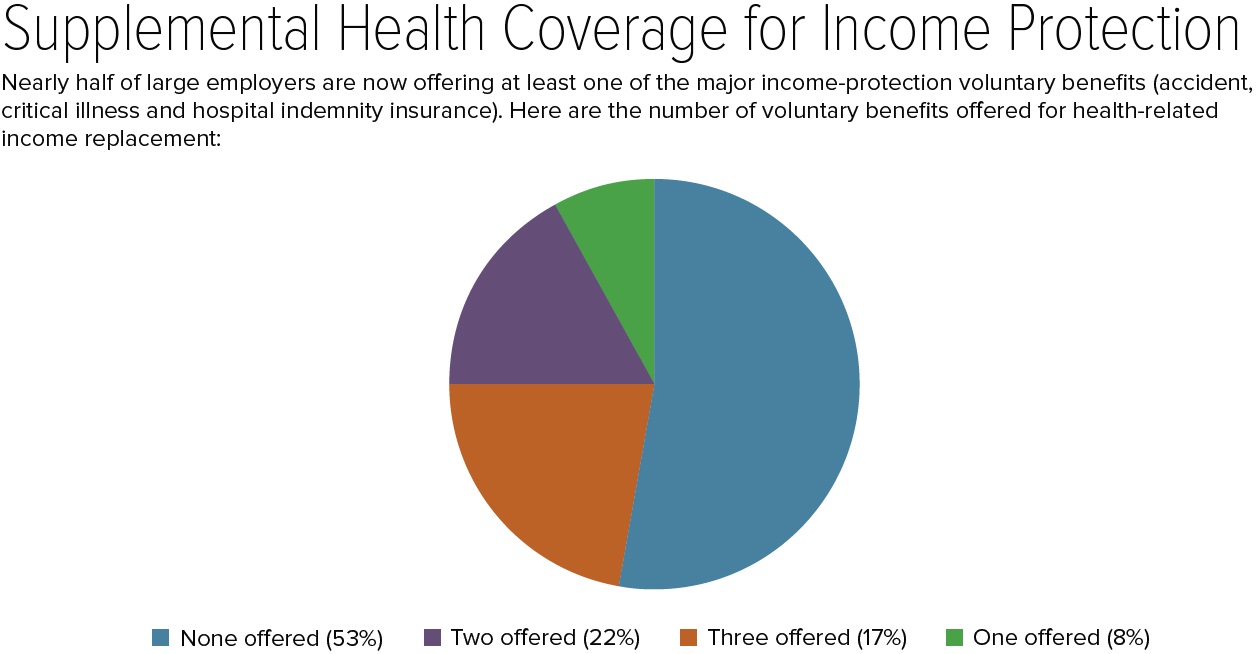

Source: Benefitfocus, The State of Employee Benefits 2017, based on enrollment data from 504 large employers with more than 1,000 full-time employees. |

"Most employers want to be as generous as possible with their employees but there's only so much they can do, given their overall business expenditures," Buckey said. "Sometimes doing as much as possible means providing an opportunity for employees to buy coverage they might not have otherwise thought of, or wouldn't have known how to go about purchasing."

However, it's by no means certain that the monthly premiums that employees pay for supplemental voluntary coverage will be less than their below-the-deductible medical costs in any given year. As with all insurance, whether to purchase voluntary coverage involves assessing how much risk reduction (to mitigate the potential of high medical expenses) an employee feels comfortable paying for.

Another consideration is that supplemental health policies could prevent an employee from being able to contribute to a health savings account (HSA), because HSAs must be linked to high-deductible plans with no reimbursement for medical expenses until the employee has paid up to the annual deductible limit (the deductible thresholds for 2018 are $1,350 for self-only coverage and $2,700 for family coverage).

[SHRM members-only how-to guide: How to Design an Employee Benefits Program]

More Choices, Sometimes More Confusion

"There's a different mindset when employees are being asked to choose benefits that they pay for themselves," said Meredith Ryan-Reid, senior vice president at insurance provider MetLife's group benefits division in New York City.

"When there are more choices, that can also be confusing, so people need help to understand what's available to them," she said.

For supplemental life insurance—one of the oldest voluntary benefits marketed to employees—"we send out communications that are customized at the employee level, offering them an opportunity to bump up coverage one more level without medical underwriting, explaining the premium rate and the increased benefits that their beneficiaries would receive, so they can make an informed decision. There's nothing fancy or digital about that; it's just actionable information [about how this benefit] might provide greater security."

She added, "it's about telling the story at the personal level so that it all makes sense."

Most Popular Voluntary Benefits

The most frequently offered health-related voluntary benefits are:

- Life insurance.

- Dental coverage (employee-paid).

- Cancer insurance.

- Critical illness insurance (internal cancer, heart attack, stroke, kidney failure, blindness, paralysis and major organ transplant).

- Disability insurance.

- Accident insurance.

Source: National Association of Health Underwriters, An Employer's Guide to Voluntary Products.

ERISA Considerations

When providing access to voluntary benefits during open enrollment, "it's important to be careful how these benefits are discussed, or you may inadvertently make your voluntary benefits an ERISA plan," regulated by the Employee Retirement Income Security Act, Buckey said.

ERISA plans face an array of reporting, disclosure and fiduciary obligations that don't apply to non-ERISA plans, explained Uche Enemchukwu, a benefits attorney and consultant at Willis Towers Watson in Chicago. The obligations include annual filing of Form 5500.

To avoid triggering ERISA, a plan must be completely voluntary and employee-paid. Employee-paid voluntary benefits, if "endorsed" by the employer, can become ERISA plans, "so be careful about posting the vendor's logo on your website" or taking steps beyond negotiating costs, communicating what the benefit is and that it's now available, and processing salary-deferred contributions, Enemchukwu advised.

"All the employer can do is allow the insurer to advertise the plan," Buckey said. "The employer can collect and send premiums to the insurer; but the employer can't receive incentive payments or direct compensation associated with the program."

While some employers are even wary about including voluntary benefits in their open enrollment guides, others think that doing so is an acceptable practice if care is taken to avoid suggesting the employer's endorsement, she noted.

However, "because you have to be careful not to be seen as endorsing the benefit or encouraging enrollment in the voluntary plan, it's helpful to have an outside party—the benefit issuer or a third-party administrator—present the benefit," Buckey added.

There's also another option. Some employees have proactively made the decision to go ahead and treat voluntary health benefits as ERISA plans, Buckey said, "because it's too much trouble to keep track of all the ways that they could inadvertently get tripped up by ERISA and then be liable for a lack of compliance."

Making the Health Plan + Voluntary Benefits Calculation

"Employee should choose their health plan last, not first," recommended Cameron Congdon, health and benefits large-market leader at Willis Towers Watson in Boston.

"Instead of comparing 2-3 health plans and selecting one—hoping it will meet their needs—employees may be better off being advised to take these steps," Congdon said:

- Assess their medical and other health, financial security, and protection needs first, using needs assessment and decision-support tools.

- "Shop" the plans recommended—both core medical and voluntary benefits.

- Figure out which of the recommended plans they can afford based on their budget, and sometimes the optimal package is the right combination of plans.

- Buy plans that are right for them that they can afford.

Consider an employee who has three core medical plan options: $500 deductible, $1,000 deductible, and $2,000 deductible

The employee's annual contributions are $2,200, $1,500 and $800, respectively.

The employee also has the choice of several voluntary plans: critical illness (flat $10,000 paid out for major illness) and hospital indemnity ($3,000 paid out if hospitalized). The combined cost of both of these coverages is less than $300 per year.

"The savvy employee could choose the core medical plan with a $2,000 deductible, purchase one or both voluntary plans, end up with coverage that reduces their financial risk from some of the big-ticket medical risks—and save the difference in contributions," Cameron said.

Example Combination Scenario Employee contribution to core medical with $2,000 deductible = $800 Cost of both voluntary plans = $300 Total contribution = $1,100 Versus: $2,200 for core medical with $500 deductible or $1,500 for core medical with $1,000 deductible.

|

This is the final installment in a five-part series of articles on meeting open enrollment challenges. The previous installment is Open Enrollment: Using Social Media and Decision-Support Tools.

Also in this series:

Part One: Open Enrollment: Active vs. Passive Benefits Election

Part Two: Open Enrollment: Developing Your Game Plan

Part Three: Open Enrollment: Targeted Communications Address Differing Needs

Related SHRM Resources:

Open Enrollment Guide & Resources Page

Related SHRM Articles:

Use Voluntary Benefits to Attract and Keep Part-Time Workers, SHRM Online Benefits, August 2017

HR Gets Strategic about Voluntary Benefits, HR Magazine, May 2014

Was this article useful? SHRM offers thousands of tools, templates and other exclusive member benefits, including compliance updates, sample policies, HR expert advice, education discounts, a growing online member community and much more. Join/Renew Now and let SHRM help you work smarter.

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.