IRS Announces 2022 Limits for HSAs and High-Deductible Health Plans

Separately, HHS released annual out-of-pocket limits for ACA-compliant plans

Update: On April 29, 2022, the IRS announced health savings account (HSA) contribution limits for 2023. See the SHRM Online article IRS Announces Spike in 2023 Limits for HSAs and High-Deductible Health Plans. |

Health savings account (HSA) contribution limits for 2022 are going up $50 for self-only coverage and $100 for family coverage, the IRS announced May 10, giving employers that sponsor high-deductible health plans (HDHPs) plenty of time to prepare for open enrollment season later this year.

The annual inflation-adjusted limit on HSA contributions will be $3,650 for self-only and $7,300 for family coverage. That's about a 1.4 percent increase from 2021.

In Revenue Procedure 2021-25, the IRS confirmed HSA contribution limits effective for calendar year 2022, along with minimum deductible and maximum out-of-pocket expenses for the HDHPs with which HSAs are paired.

"For HSA-qualified insurance plans, the minimum deductibles will remain the same as for 2021, but the annual out-of-pocket maximums will increase slightly for 2022," said Roy Ramthun, president and founder of HSA Consulting Services. This means health plans do not need to substantially change their plan designs for 2022.

| Contribution and Out-of-Pocket Limits for Health Savings Accounts and High-Deductible Health Plans | |||

|---|---|---|---|

| 2022 | 2021 | Change | |

| HSA contribution limit (employer + employee) | Self-only: $3,650 Family: $7,300 | Self-only: $3,600 Family: $7,200 | Self-only: +$50 Family: +$100 |

| HSA catch-up contributions (age 55 or older) | $1,000 | $1,000 | No change |

| HDHP minimum deductibles | Self-only: $1,400 Family: $2,800 | Self-only: $1,400 Family: $2,800 | No change No change |

| HDHP maximum out-of-pocket amounts (deductibles, co-payments and other amounts, but not premiums) | Self-only: $7,050 Family: $14,100 | Self-only: $7,000 Family: $14,000 | Self-only: +$50 Family: +$100 |

| Source: IRS, Revenue Procedure 2021-25. | |||

Adjustments Reflect Inflation

Contribution limits for various tax-advantaged accounts for the following year are usually announced in October, "except for HSAs, which come out in the latter part of April or May," explained Harry Sit, CEBS, who writes The Finance Buff blog. The contribution limits are adjusted for inflation (rounded to the nearest $50) annually, using the Consumer Price Index for All Urban Consumers for the 12-month period ending on March 31. The catch-up contribution amount, however, is fixed by statute.

HSA and HDHP limit increases "are released much earlier than other employee benefit limits so that insurance companies that offer high deductible health plans—which participants must enrolled in to make HSA contributions—can get their insurance products approved by state insurance regulators," explained William Sweetnam, legislative and technical director at the Employers Council on Flexible Compensation (ECFC), which represents sponsors of account-based benefits plans.

"The family coverage numbers happened to be twice the individual coverage numbers in recent years but it isn’t always true," Sit pointed out. "Because the individual coverage limit and the family coverage limit are both rounded to the nearest $50, when one number rounds up and the other number rounds down, the family coverage limit can be slightly more or slightly less than twice the individual coverage limit."

Catch-Up and Family Member Contributions

HSA holders age 55 or older by the end of the year—not age 50, as with 401(k) and individual retirement account (IRA) catch-up contributions—can contribute an additional $1,000 to their HSAs.

However, "because an HSA is in one individual's name, just like an IRA—there is no joint HSA even when you have family coverage—only the person age 55 or older can contribute the additional $1,000 in his or her own name," Sit said. If only one spouse is 55 or older but the younger spouse contributes the full family contribution limit to the HSA in his or her name, the older spouse has to open a separate account to make the additional $1,000 catch-up contribution. If both spouses are age 55 or older, "they must have two HSA accounts in separate names if they want to contribute the maximum," Sit noted.

Another point about family contributions: "If your HDHP also covers your adult children who are not claimed as a dependent on your tax return, they can also contribute to an HSA in their own name if they don't have other non-HDHP coverage," Sit added, however "they will have to open an HSA on their own with an HSA provider."

ACA's Limits Differ

There are two sets of limits on out-of-pocket expenses for health plans, determined annually by federal agencies, which can be a source of confusion for plan administrators.

The Department of Health and Human Services (HHS) establishes annual out-of-pocket or cost-sharing limits under the ACA for essential health benefits covered under an ACA-compliant plan, excluding grandfathered plans.

On April 30, HHS released the Notice of Benefit and Payment Parameters final rule for 2022, published in the May 5 Federal Register. According to an HHS press release, the annual payment notice makes regulatory changes in the individual and small-group health insurance markets, and outlines parameters and requirements issuers need to design plans and set rates for the upcoming plan year.

The HHS's annual out-of-pocket limits are higher than those set by the IRS. To qualify as an HSA-compatible HDHP, a plan must not exceed the IRS's lower out-of-pocket maximums.

Below is a comparison of the two sets of limits:

| 2022 | 2021 |

Maximum out-of-pocket for ACA-compliant plans (HHS) | Self-only: $8,700 Family: $17,400 | Self-only: $8,550 Family: $17,100 |

| Family: $14,100 | Family: $14,000 |

The HHS final maximum out of pocket (OOP) limit includes the plan's deductible and cost sharing for essential health benefits (EHBs) under the ACA, wrote Mark Holloway, senior vice president and director of compliance services at Lockton Companies, a benefits broker and services firm. "Self-insured plans and large-group insured plans are not required to cover all EHBs (although small-group insured plans are), but to the extent the plans do cover an EHB … OOP expenses for in-network EHBs must accumulate against the maximum OOP limit" and the plan may not impose annual or lifetime dollar limits on EHBs.

HDHPs and Embedded Individual OOP Limits

As of the beginning of the 2016 plan year, guidance from the HHS, DOL and IRS required that non-grandfathered plans must apply the ACA (non-HDHP) individual maximum OOP limit to individuals enrolled in family coverage under either a non-HDHP or an HDHP. "This requires each enrollee to have his or her own individual OOP limit on essential health benefits that is no higher than the maximum self-only OOP limit," Holloway explained.

In practice, this means that:

- If an individual has self-only coverage under an HDHP in 2022, the HDHP individual maximum OOP applies ($7,050) and any HDHP individual deductible.

- If an individual has family coverage under an HDHP in 2022, the non-HDHP individual maximum OOP applies ($8,700), as well as the family HDHP maximum OOP ($14,100) and any HDHP family deductible. In some cases, this will mean that the plan must start paying 100 percent for one family member even though the family deductible or family maximum OOP has not been met.

Excepted Benefit HRA Limit Unchanged

IRS Revenue Procedure 2021-25 also states that the maximum amount that employers may contribute for excepted benefit health reimbursement arrangements (excepted benefit HRAs) for plans years beginning in 2022 will remain at $1,800.

Employers use excepted benefit HRAs to help cover the cost of employees' vision, dental, or short-term, limited-duration insurance plan premiums.

Tax code regulations provide that, for each plan year, amounts newly made available to excepted benefit HRAs cannot exceed $1,800. For plan years beginning after Dec. 31, 2020, the $1,800 amount is adjusted for inflation by an amount equal to $1,800 multiplied by the applicable cost-of-living adjustment. Any increase that's not a multiple of $50 is rounded down to the next lowest multiple of $50.

Because of this indexing methodology, the maximum new-contribution amount for an excepted benefit HRA remained at $1,800 for 2021 and will do so again for the 2022 plan year.

Contributing to the HSA Cap Pays Off Making payroll contributions up to the annual HSA limit, when participants are able to do so, can provide extra savings to pay for post-retirement health care. According to Fidelity Investments, which manages retirement accounts and HSAs, a 65-year old couple retiring this year can expect to spend $300,000 in health care and medical expenses throughout retirement, even when enrolled in Medicare. For single retirees, the 2021 estimate is $157,000 for women and $143,000 for men. "We continue to see many HSA owners not using these accounts to their full potential, in particular not using the power of investing to potentially grow their savings. And that's the step that can make a big difference, especially for younger people with time on their side," said Hope Manion, senior vice president at Fidelity Workplace Consulting. At the start of the year, 16.5 percent of Fidelity HSAs had at least some funds invested in mutual funds, an increase from 11.2 percent at the beginning of 2020. Fidelity's 1.76 million funded HSAs hold $10.2 billion in total assets. Fidelity calculates that a couple who contributes the maximum family limit to an HSA, withdraws 50 percent each year to pay for current qualified medical expenses but leaves the remaining 50 percent invested and earning an average 7 percent return, would have the potential to grow the account to $300,000 after about 25 years, reaching nearly half a million dollars after 30 years. |

Educate Employees on FICA Savings

HSAs are one of the only tax-advantaged accounts that exclude contributions not only from income tax but also from FICA payroll taxes, noted Voya Financial, which manages HSAs and retirement plan accounts.

The FICA tax rate for both employers and employees is 7.65 percent, of which 6.2 percent helps to fund Social Security while the remaining 1.45 percent goes to Medicare.

"Even pretax 401(k) contributions are still subject to FICA taxes," unlike HSAs, Voya pointed out. "And though IRA contributions can be described as 'before-tax,' employees have already paid FICA taxes on those contributions."

Advanced Planning

The 2022 limits are "good to know for planning purposes," ECFC's Sweetnam said, "Employers generally start talking to their employees about making health care choices, and about these limits, during open enrollment season after the end of summer."

But it's not too early to plan ahead. "Employers are advised to begin updating payroll and plan administration systems to reflect the 2022 cost-of-living adjustments," advised the Boston-based Wagner Law Group. "In addition, employers should incorporate the 2022 HSA limits into all relevant participant communications, such as open enrollment and communication materials, plan documents and summary plan descriptions."

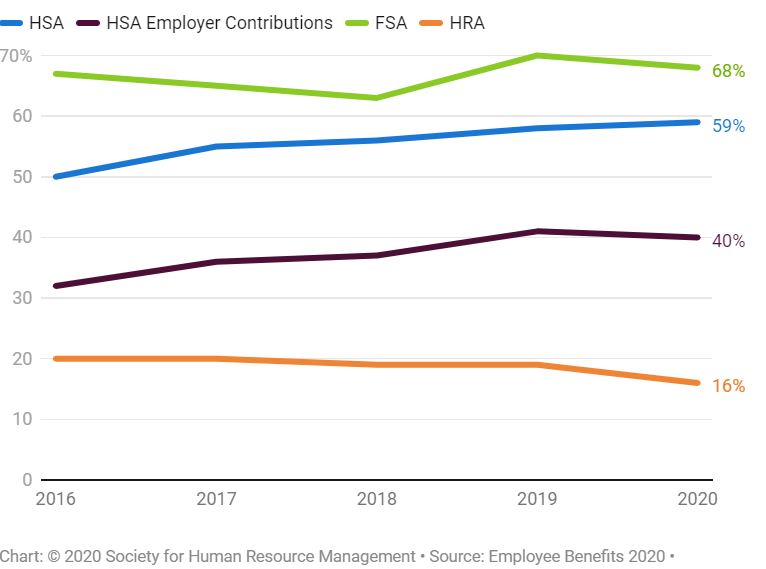

More Employers Offering HSAs HSAs continue to become more prevalent as an employee benefit while use-it-or-lose-it flexible spending accounts (FSAs)—still the most common vehicle for letting employees use pretax dollars for health expenses—and employer-funded HRAs have declined. In the Society for Human Resource Management's 2020 Employee Benefits survey, based on responses from 2,504 HR professionals across the U.S., collected from Sept. 29 through Nov. 10, 2020, HSAs were offered by 59 percent of respondents' organizations. Two thirds of organizations that offered HSAs (representing 40 percent of survey respondents overall) contributed to employees' HSAs. |

Related SHRM Articles:

An Early Release of 2023 Out-of-Pocket Limits for Non-HSA Plans, SHRM Online, February 2022

2022 Benefit Plan Limits & Thresholds Chart, SHRM Online, November 2021

2022 Health FSA Contribution Cap Rises to $2,850, SHRM Online, November 2021

For 2022, 401(k) Contribution Limit Rises to $20,500, SHRM Online, November 2021

2022 Wage Cap Rises to $147,000 for Social Security Payroll Taxes, SHRM Online, October 2021

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.