Targeted Benefits Help Baby Boomers Stay at Work, Prepare to Retire

Part 2: Flexible schedules, retirement planning and support groups aid older workers

Part 1

Easing into Retirement

Part 2

Targeted Benefits for Aging Workers

Employers who offer benefits specifically for older workers have two goals: to help their older employees stay at work longer and prepare them to leave when the time is right. That's because some older workers are still at the top of their game, with experience and skills that would be hard to replace, while others may have already "retired in place," signaled by a loss of interest in their work and a drop in productivity.

Lauren Hoeck, senior director of retirement consulting at Willis Towers Watson in Washington, D.C., said employers should be mindful of both these challenges by offering benefits that address:

- The loss of knowledge and skills when too many high-value workers leave for good.

- The problems that arise when older workers delay retirement and are just hanging on.

When workers who should retire don't, the problems that arise "include higher costs of benefits and pay for these employees and deferred opportunities for midcareer employees," Hoeck noted.

But don't write off all older workers, as many are engaged and productive and contribute to their organization in ways that more than justify their higher salaries and costs—although they may need some support to continue doing so.

Flex Arrangements Help

To keep valued older workers on board, some employers allow them to change positions, for example by stepping down from a managerial role into an individual contributor role, and shift to part-time or part-year employment opportunities. Others offer phased retirement programs.

"Employers are offering part-time work or the opportunity to come back as a contractor for older employees they want to keep," said Jeanne Thompson, head of workplace solutions thought leadership at Fidelity Investments in Boston. "If [older workers] want to continue to work, they may be offered the opportunity to do so for three days a week from home or with a reduced, 30-hours-per-week schedule."

Hoeck suggested, "Employers can also modify working conditions to conform to preferences of older employees by looking at things like ergonomic workspaces."

When to Hold, When to Fold

However, helping other aging workers prepare for the next phase in their lives may be about "helping them see that maybe it's time" to retire, Thompson said.

Sean Nehlsen, Cleveland-based regional managing director of HR consulting services with OneDigital, pointed out that "older workers have a wealth of knowledge and experience and often will outwork younger colleagues. But when they reach the point where they're working only to make a paycheck or to keep their benefits, they can lose that drive and productivity at work. Employers need to be aware of that and to provide tools, resources and advice to help them retire."

That's often not what employers are doing, however. Some 66 percent of retirees said their most recent employers did nothing to help with their transition to retirement, and another 16 percent were not sure how their employers helped, according to a 2018 survey of more than 2,000 retirees conducted by nonprofit Transamerica Center for Retirement Studies (TCRS).

[SHRM members-only toolkit: Designing and Managing Flexible Benefits (Cafeteria) Plans]

Savings Checkups

Employees won't retire if they're uncertain they can afford to do so, and their fears are significant.

A new study from American Century Investments of 1,500 full-time workers found that among their concerns about retiring, workers are most worried about outliving their money.

"Despite the all-too-real challenge of saving, many workers are overlooking opportunities that could help improve their long-term financial situation," said Catherine Collinson, CEO and president of TCRS in Los Angeles. "Small steps, such as using a retirement calculator to estimate savings needs, engaging in financial planning, creating a budget, formulating a retirement strategy and learning about retirement investing can make a big difference in the long run."

If employees are staying in the workforce longer, "it's often because they don't have enough retirement savings," Nehlsen said. He has seen many employees, as their reach their 50s and 60s, "with outstanding 401(k) loans, and their account balances are minimal. They're putting in 2 percent or 3 percent of their paycheck," whereas many retirement advisors recommend a career-long contribution rate of at least 15 percent of pay, which includes the employer's contribution, to save enough for a secure retirement.

Thompson said, "We're starting to see more employers offer retirement income planning, often by holding workshops and one-on-one sessions," to help employees determine if they've saved enough, when they should claim Social Security and how to set up a plan for drawing down assets to create retirement income. (This topic is addressed in the next installment of this series, "Helping Employees Turn Retirement Plan Savings into Lifetime Income.")

Many of the firms that provide services to 401(k) plans offer this aid, along with online calculators and other tools to gauge retirement savings and develop account withdrawal strategies, Nehlsen said. "Even at small to midsize companies, these benefits are available to employees, but often older workers don't know about them and so aren't taking advantage of them."

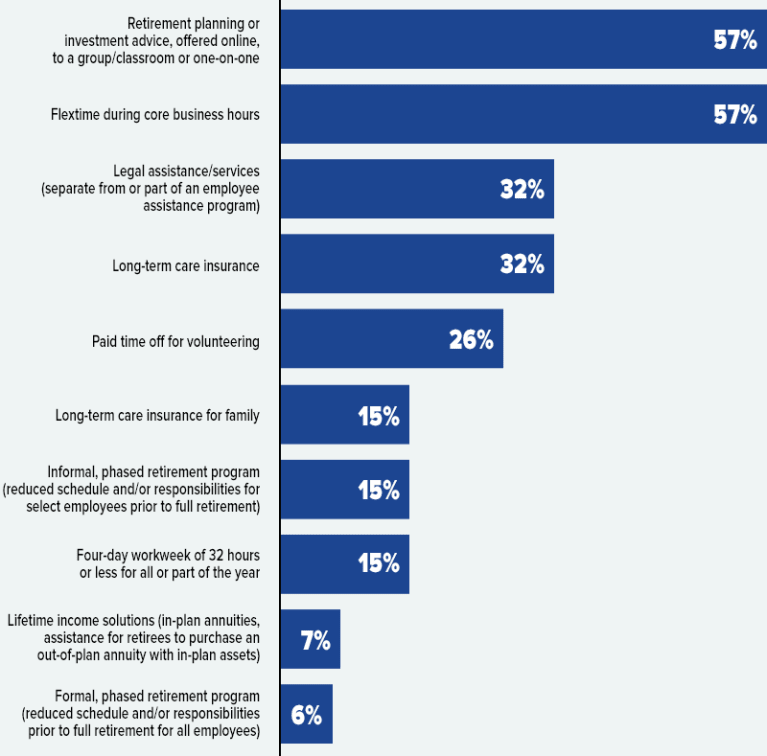

Benefits That Address the Needs of Older Workers

The percentage of organizations that offer employees the following benefits, which can be helpful for aging workers.

Source: The Society for Human Resource Management's 2019 Employee Benefits survey, with responses from 2,763 HR professionals.

A Last Chance to Transfer Knowledge

Workers who retire may later find they're bored and want to go back to work. "They're not looking to get back into their previous roles and work 40 hours, 9 to 5," Nehlsen said. "They're asking, 'Is there a project I can help with or a couple weeks' work here and there?' just to stay involved."

Returning on a limited basis is also a chance to let older workers pass along their knowledge and experience, Nehlsen said. "If you can get them back into the office for five to 10 hours a week, just having that knowledge in the workplace can be critical."

PART 3: Lifetime Income Prospects

| Related SHRM Articles: Employers Make Strides in Retirement Security, Though Gaps Persist, SHRM Online, July 2018 Preparing for an Aging Workforce: Strategies, Templates and Tools for HR Professionals, SHRM Research Guide, 2016 |

Related Articles

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.