More Small and Midsize Firms Choose to Self-Insure

Avoiding some Affordable Care Act requirements and fees may be a factor

Update: Self-Insurance Trends Through 2016 In 2016, 40.7 percent of private-sector employers reported that they self-insured at least one of their health plans, up from 29.7 percent in 2000, the Employee Benefit Research Institute reported in February 2018. From 2013 to 2016, the percentage of employers by size that offered at least one self-insured plan changed as follows:

|

A growing number of small and midsize employers are opting to self-insure their employee health plans, in part because self-insuring allows employers to avoid some—but by no means all—of the coverage mandates and administrative costs imposed by the Affordable Care Act (ACA).

While the data do not conclusively demonstrate that ACA is the reason for this shift, the findings "are consistent with the prediction that the ACA would cause more small- and midsized employers to adopt self-insured plans," said Paul Fronstin, health research director at the nonprofit Employee Benefit Research Institute (EBRI) in Washington, D.C., and author of EBRI's July report on self-insured health plan trends.

Employer-sponsored group health plans fall into two categories:

- Fully insured plans. Employers pay premiums to an insurance company, which then pays health care providers for enrollees' claims based on the coverage benefits outlined in the plan.

- Self-insured (or self-funded) plans. Employers keep the plan premiums and pay the actual cost of the claims themselves, contracting with an insurance company or another third-party administrator (TPA) to design the plan, process claims and provide administrative services. Self-insured employers, especially smaller ones, often purchase a separate stop-loss policy (or "reinsurance") from an insurance company to cover extremely large claims.

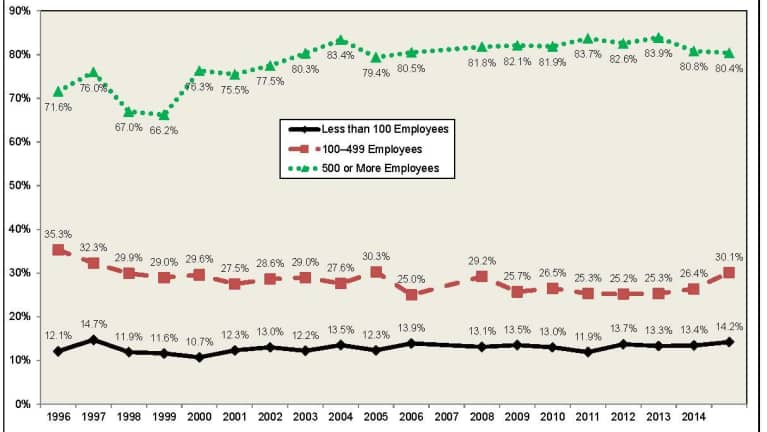

Among the new findings from the EBRI report, from 1996 to 2015 the percentage of U.S. private-sector employers offering at least one self-insured health plan rose from 28.5 percent to 39 percent.

From 2013 to 2015, the percentage of employers by size that offered at least one self-insured plan changed as follows:

- Small employers (fewer than 100 employees)—rose to 14.2 percent from 13.3.

- Midsize employers (100 to 499 employees)—rose to 30.1 percent from 25.3 percent.

- Large employers (500 or more employees)—fellto 80.4 percent from 83.9 percent.

Percentage of Private-Sector Employers that Self-Insure at Least One Plan, by Firm Size, 1996-2015

(Click on the graphic to view a larger version.)

"Key provisions of the ACA took effect in 2013, which is why the analysis focuses on the period between then and 2015," Fronstin noted. "These data are consistent with the perspective … that the ACA would cause more small and midsized employers to adopt self-insured plans."

The EBRI report draws on data from private- and public-sector employers collected by the U.S. Census Bureau for the Agency for Healthcare Research and Quality.

Fewer Regulatory Burdens

One example of how the ACA can limit flexibility and drive up costs for small businesses involves "essential health benefits."

The ACA identifies 10 benefit categories that must be included as essential health benefits for fully insured small-group market plans. But self-insured plans, along with coverage offered in the large-group market and through grandfathered plans, are not required to cover each of these essential health benefits. (All plans, however, must still meet the ACA's requirements to provide "affordable" coverage that offers at least "minimum value.")

"When [self-funded arrangements are] properly designed, there are several ways an employer can 'win,' " noted Sean McGuire, CEO of E.D. Bellis, a benefits compliance and consulting firm in Omaha, Neb., in a recent online post. "Examples … include eliminating community rating, avoiding essential health benefit mandates required by the ACA and perhaps most importantly, the avoidance of adverse selection in the fully insured marketplace."

In addition, organizations that self-insure retain the claim reserves traditionally held by insurance companies and keep the interest on those reserves, McGuire said.

Beware Financial Risks

Bob Graboyes, senior fellow for health and economics at the National Federation of Independent Business, a small business advocacy group, recently wrote that "With self-insurance, certain businesses save money in most years, losing money in the scattered years when some employees suffer major illnesses. For these businesses, self-insurance costs less over the long-run than do fully insured products. So some, but not all, businesses will find it advantageous to self-insure."

Striking a more cautious note, Robert Pozen, former chairman of MFS Investment Management, warned that "For small businesses subject to the [ACA's] employer mandate, self-funding offers both great advantages and some treacherous disadvantages." Among the latter, Pozen noted that "Since stop-loss policies are issued on an annual basis without guaranteed renewal, an unexpected rise in the health care costs at a small firm can lead to much higher premiums the following year or an abrupt cancellation of the policy altogether."

He suggested that "a potentially crippling scenario for a small business is not far-fetched. Say an employee is diagnosed with an obscure type of cancer. He needs intensive therapy for two to three years at a cost of millions of dollars. The stop-loss insurer may pay for his care for one year then decline to renew the contract. No other reinsurer will take on the policy, so the employer gets stuck with the bill. For many small businesses, that would be financially devastating."

Related SHRM Articles:

Self-Insurance Is Just the Start, Say Health Plan Innovators, SHRM Online Benefits, April 2018

Small Businesses Are Dropping Health Coverage; Large Employers Hold Steady, SHRM Online Benefits, July 2016

Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.