Small Businesses Are Dropping Health Coverage; Large Employers Hold Steady

Whether to continue employer-provided coverage depends on the facts and circumstances of a given employer, even in the small market

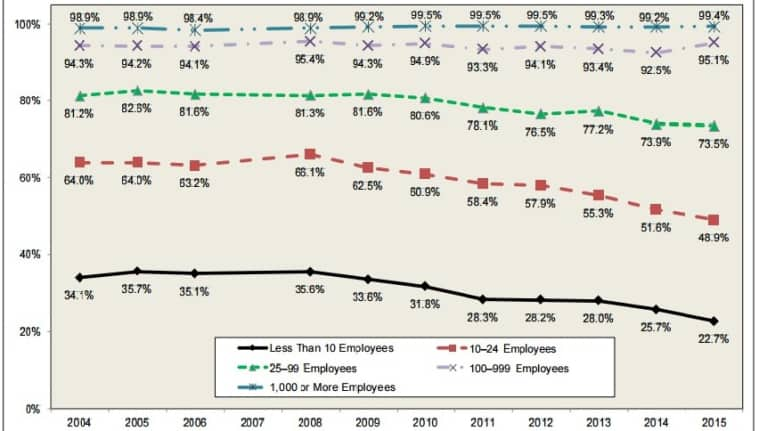

In the wake of the Affordable Care Act (ACA), fewer small employers are offering health benefits to their workers. Big employers, however, have overwhelmingly continued to provide health coverage.

An analysis published in July by the nonprofit Employee Benefit Research Institute (EBRI) in Washington, D.C., examined the percentage of employers offering health insurance since 2004, in order to better understand how health insurance offer rates have been affected by the ACA and the recession of 2007-09. The data come from the federal Medical Expenditure Panel Survey overseen by the Department of Health and Human Services.

Among larger employers, health insurance offer rates—the percentage of employers offering health insurance benefits to their workers—have held steady:

- For employers with 1,000 or more employees, around 99 percent offered health coverage from 2004 through 2015.

- For employers with 100 to 999 employees, the range offering health coverage has varied only slightly, from around 93 to 95 percent.

But health coverage among smaller employers has been falling in recent years. From 2008 to 2015, offer rates at small organizations declined as follows:

- For employers with fewer than 10 employees, from 35.6 percent to 22.7 percent (a 36 percent dip).

- *For employers with 10 to 24 employees, from 66.1 percent to 48.9 percent (a 26 percent dip).

- *For employers with 25 to 99 employees, from 81.3 percent to 73.5 percent (a 10 percent dip).

Percent of Private-Sector Employers that Offer Health Insurance, 2004-2015

(Click on the graphic to view a larger version.)

"Historically, smaller employers have been less committed to sponsoring health coverage than larger employers," said Paul Fronstin, EBRI's director of health research and author of the study. "One often-cited reason is that smaller firms, more than larger ones, frequently face higher and more volatile increases in health insurance premiums," he explained.

When the 2007-09 recession took hold and unemployment rates in the U.S. rose to around 10 percent, "many smaller employers that had been sponsoring health plans dropped their coverage," Fronstin said. Small-employer sponsorship continued to decline after 2009 as business and labor/employment softness and uncertainty continued, he added.

Higher Costs, Newer Options

Enactment of the ACA in 2010 appears to have persuaded many small employers to stop insuring their employees' health care.

The ACA's "shared responsibility" mandate to provide health coverage or face steep penalties only applies to employers with 50 or more full-time employees or part-time equivalents. However, if small employers choose to provide health coverage, they must offer plans that meet the ACA's specifications for the small-group market, including coverage of essential health benefits, and they must satisfy the ACA's general requirements to be affordable and provide at least minimum value to employees.

According to the EBRI analysis:

- The ACA requirements could have convinced many employers that health plan sponsorship would become a more regulated and expensive benefit—and therefore something to stay away from.

- Workers at smaller firms can purchase health coverage in the ACA's public exchanges, where subsidies are available for those with incomes below 400 percent of the federal poverty level.

Facing a challenging business environment, many small employers may have decided that the increasing costs and risks associated with offering health coverage were no longer justified, given that employees could now purchase coverage on a public exchange, Fronstin concluded.

Small-Group Market Challenges

The ACA's incentives for small businesses to provide health benefits have proved ineffective. The Small Employer Health Care Tax Credit has gone largely unused due to what small business owners describe as confusing rules and burdensome requirements. Likewise, the delayed and stunted rollout of the ACA's Small Business Health Options Program (SHOP) exchanges and the limited SHOP plans available in many states, along with the continued phase-out of grandfathered plans, have all worked against small business coverage.

Nevertheless, the majority of small employers still believe that offering health insurance is important to recruiting and retaining good employees, said Erin McGinty, director of benefits consulting at TriNet, an HR services and benefits administration firm based in San Leandro, Calif.

"While the philosophy of offering benefits to attract and retain top talent does not align with the declining number of small firms offering health insurance, there is likely good reason," McGinty said. "The ACA's small-group market reforms can be confusing and not necessarily helpful to small businesses."

Companies with fewer than 50 full-time employees (or, in some states, fewer than 100 full-time employees) "are no longer able to participate in their state's large-group plans, which generally provide companies with more flexibility than small-group plans," she said. Small-group plans are being brought into the same classification used for plans available in the ACA marketplace, "so a company with 45 employees would be offering the same plan designs as a company with five employees," McGinty said.

Small-group plans also face greater restrictions on underwriting and plan pricing, she noted.

Cost-Benefit Calculation

When small businesses that aren't subject to the ACA's shared responsibility penalties decide whether to maintain or drop coverage, they should consider if their employees are entitled to subsidized coverage through a public exchange, said Mike Thompson, president and CEO of the nonprofit National Business Coalition on Health, based in Washington, D.C.

"Few large employers have concluded that it's in their best interest to drop coverage, but the same economics don't always apply to small employers," Thompson explained. Small businesses "may find that employees earning at the low end can get heavily subsidized coverage in the open market that will be as attractive and potentially more attractive then coverage that the employer could provide."

If employees are likely to receive subsidized coverage through a public exchange, "that could mitigate concerns about being able to compete with other employers that do offer health coverage," Thompson said. "If at the end of the day you can get comfortable that your employees are going to have access to good coverage through the exchanges, then that option may make sense."

Employers who choose to drop coverage should take steps to help their employees navigate the ACA's marketplace, Thompson said, and should educate them about the options available for subsidized coverage.

However, he added, "if your business generally has higher-income employees, you'll probably find a need to offer coverage to compete for that talent," as the exchange-based coverage available to those employees "may not be as heavily subsidized—or subsidized at all—nor as rich as they would normally receive through employer-provided benefits. So this decision is geared by the economics of the business and the nature of the people that you're employing."

Employers can provide health coverage on a tax-excluded basis, while the same amount of money spent on salaries would be taxable, Thompson pointed out. If employees are not earning at the lower-end range for which exchange-based plans are subsidized, "it can be to your benefit to provide the coverage and use that as a competitive advantage to attract the talent that you need to run your business."

And if employees are not entitled to subsidized coverage, "you have to think about paying them more, and if you do pay them more, you need to consider that this higher income is taxable as opposed to an employer-provided health benefit. Now you're situation is closer to that of large employers that haven't found it beneficial to stop providing coverage."

In short, "Whether it makes sense to continue offering employer-provided plans will depend on the facts and circumstances of a given employer, even in the small market."

An additional concern: Among the biggest national insurers, Aetna announced it intends to limit is participation on the ACA's public exchanges, following a move by UnitedHealthcare to withdraw from most exchanges. If this trend continues, employees buying policies on the exchanges may find fewer choices and higher prices.

A PEO Alternative

"A viable solution for small businesses that want the variety in plan design and pricing that they've enjoyed in the past is to look at outsourcing to a PEO [professional employer organization], where they can reap the benefits of the large-group market," McGinty suggested.

PEOs, which hire a business's employees and then charge the business for payroll, benefits and other HR support, now service between 156,000 and 180,000 small and midsize enterprises, according to the National Association of Professional Employer Organizations (NAPEO) in Alexandria, Va. The PEO industry has been adding, on average, roughly 100,000 worksite employees and 6,000 new employer clients annually, NAPEO's website reports.

"A PEO can simplify benefits administration but the fundamental economics don't necessarily change," said Thompson. "A PEO might be able to buy better coverage on behalf of that employer, but when comparing employer-provided benefits versus allowing employees to purchase subsidized plans through an exchange, the over-arching economics are still driven by the demographics and income of the workforce."

|

A Slowing Trajectory? Despite the overall trend reported by EBRI's researchers, some small companies that dropped group health insurance for their employees are reversing course, driven by a tightening labor market and rising costs and fewer choices for individual coverage, the Wall Street Journal reports. Michael Stahl, a senior vice president at HealthMarkets Inc., an agency that works with small businesses across the country, told the paper that most small businesses making changes continue to shift to individual coverage because their workers are eligible for significant government subsidies. "But the trajectory of that is slowing," he said. For the first time, "we are seeing a reverse migration back from individual to group." |

Related SHRM Article:

Small and Midsize Firms Choose to Self-Insure, SHRM Online Benefits, July 2016Was this resource helpful?

Validate your HR expertise

Earning your SHRM-CP credential makes you a recognized expert and leader in the HR field.

Related Content

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.