Many Older Workers Would Prefer to Ease into Retirement

Part 1: Employers offer phased retirement—but only to some employees

Part 1

Easing into Retirement

Targeted Benefits for Aging Workers

Older employees are looking to their employers for assistance as they see the unknowns of retirement fast approaching. If they're lucky, they'll be offered benefits that help them stay on the job until they're ready for their retirement party, along with guidance on planning for a future beyond the 9-to-5 world of work.

Benefits available to older employees will vary based on the challenges that employers need to address. Some organizations want to give younger workers opportunities to move up, making retirement coaching for older workers paramount. Others may fear a brain drain as Baby Boomers depart en masse, so offering flexible hours and encouraging the transfer of knowledge to younger colleagues is their priority. In all cases, however, finding the right benefit strategy for aging employees means understanding both the organization's talent challenges and employees' needs.

SHRM Online begins this series by looking at a benefit that many older workers say they want but most are not offered: the ability to stay at work with fewer hours and reduced responsibilities as a prelude to full retirement.

A Longer Goodbye

Phased retirement is an employer-based program that allows older workers to reduce their working hours and transition into retirement. These programs may include a partial drawdown of funds from defined contribution or defined benefit retirement plans and continuing employer-sponsored health coverage.

"Older workers may be tired of dealing with their current level of responsibility and are looking for less-stressful roles or roles that are project-based, where their schedules can be more flexible," said Sean Nehlsen, Cleveland-based regional managing director at OneDigital, an HR services provider.

Phased retirements also can allow time for older workers to share their knowledge with other employees, Nehlsen said. "When employees announce that they're ready to retire, it's too late to do any transfer of knowledge," he noted, which is why forward-looking organizations are more likely than others to offer phased retirement opportunities.

Still a Rare Benefit

For many workers, easing into retirement is an expectation that is never realized.

Among workers in the U.S. ages 61 to 66, roughly 29 percent said they had planned to reduce their work hours as they transitioned to retirement, but fewer than 15 percent subsequently reported that they were partially retired or were gradually retiring from their jobs, according to a 2017 report by the U.S. Government Accountability Office. The agency relied on the University of Michigan's biennial Health and Retirement Study of Americans over age 50, which had more than 12,000 respondents.

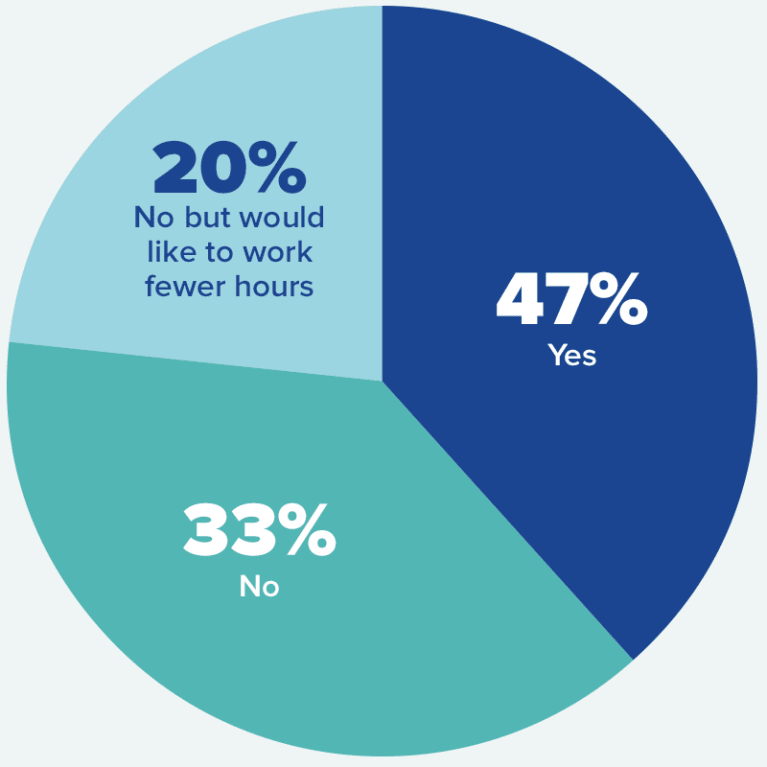

An August 2019 survey by Provision Living, a provider of senior living communities, found that among 1,032 working seniors ages 65 and older, 20 percent wanted to stay employed but cut back their hours.

WANTED: FEWER WORKING HOURS

A survey asked 1,032 working seniors ages 65 to 85 (with an average age of 67) if they'd like to retire.

Do Working Seniors Wish They Were Retired?

More than 60 percent said the decision to keep working was based on finances, while 38 percent said staying at work was a personal decision, for instance because they enjoy working or want to avoid boredom.

Source: Provision Living poll conducted in August 2019.

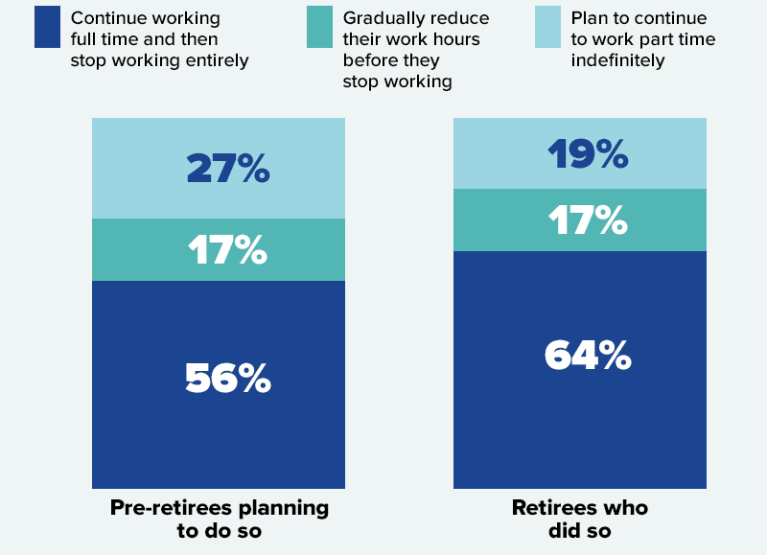

Other research shows that among pre-retirees with higher-than-average household savings, about 17 percent expected to phase into retirement, and among those recently retired, the same percentage reported actually doing so. That's according to the LIMRA Secure Retirement Institute, which provides consumer research for the retirement industry. LIMRA's survey was conducted last November, with 995 responses among adults ages 55 to 71, including those nearing retirement and recently retired.

ENTERING RETIREMENT: EXPECTATIONS AND EXPERIENCES

Older employees who are planning to keep working may find that their expectations are overly optimistic, according to a recent report by the LIMRA Secure Retirement Institute. About 1,000 people ages 55 to 71 with at least $100,000 in household assets and who have retired within the past two years or plan to retire in the next two years were surveyed.

Source: LIMRA Secure Retirement Institute 2019 report, Journey Chronicles: Transition Experiences of Work in Retirement.

Formal vs. Informal Programs

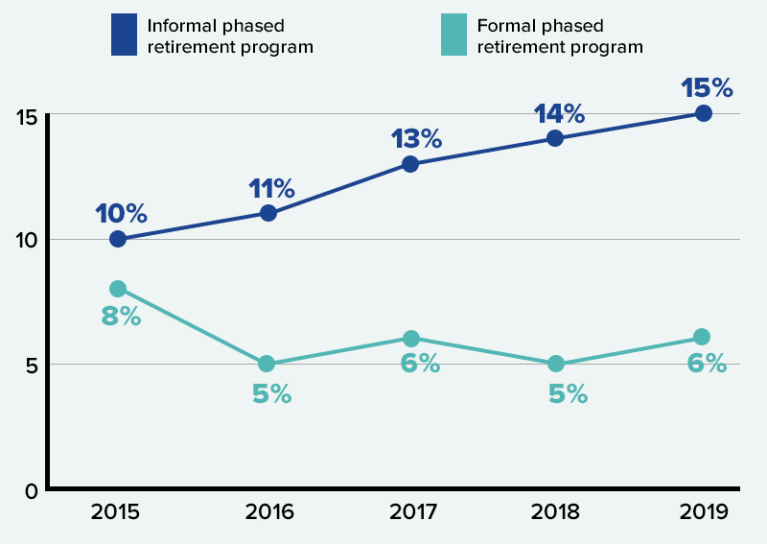

The availability of phased retirement is increasing—albeit slowly and often only for most-valued employees. Among employers that responded to the Society for Human Resource Management's 2019 Employee Benefits survey, the share of organizations offering some employees the option to phase into retirement through an informal program has risen steadily in recent years, reaching 15 percent. The prevalence of formal, phased retirement programs broadly available to workers, meanwhile, has stalled at around 6 percent, according to the survey, which was conducted earlier this year and drew responses from 2,763 HR professionals.

FORMAL AND INFORMAL PHASED RETIREMENT PROGRAMS

The share of employers offering some employees the option to phase retirement through an informal program has risen steadily in recent years, according to the Society for Human Resource Management's 2019 Employee Benefits survey. The share of employers that offer a formal, phased retirement program, meanwhile, has stalled at around 6 percent.

Source: Society for Human Resource Management, 2019 Employee Benefits survey.

Employers, the data suggest, prefer to limit phased retirement opportunities to high-performers and those with in-demand skills—which they can more easily do ad hoc. But that could lead to charges of discrimination, based on who is offered the right to shift to part-time work, although this hasn't yet been tested in the courts, benefit specialists say.

Large U.S. corporations offer phased retirement programs at a slightly higher rate than small and midsize firms. Consultancy Willis Towers Watson's 2018 U.S. Longer Working Careers Survey, completed by 143 large companies that employ 2.9 million workers collectively, found that 9 percent of respondents offered a formal, phased retirement program, but 23 percent were considering doing so. Reasons cited for not offering a formal program included administrative and compliance complexities, as well as a preference for informal and more-targeted approaches.

Among these large corporations, the survey revealed, "14 percent frequently and 41 percent sometimes have employees phase into retirement on an informal or case-by-case basis," said Lauren Hoeck, senior director of retirement consulting at Willis Towers Watson. "The types of employees targeted by these approaches included those in professional, technical and manager positions more often than those in routine and manual positions."

A Gender Split

LIMRA's survey found that women are more likely to phase into retirement than men, including those in formal and informal programs. Twenty-five percent of female recent retirees phased into retirement versus 16 percent of male recent retirees, LIMRA found.

"Men may be less likely to phase into retirement because it is more difficult to do so with their pre-retirement job functions," the researchers noted. For instance, 23 percent of men worked in managerial jobs before retirement, compared with 13 percent of women.

Phased Retirement Lite

Many employers that are hesitant to provide phased retirement opportunities are nonetheless providing flexible arrangements to allow older workers to change positions, for example by stepping down from a managerial role to a role as an individual contributor, Hoeck said.

A December 2018 survey of more than 1,800 employers by the nonprofit Transamerica Center for Retirement Studies (TCRS) found that to help employees transition to retirement, 21 percent of organizations enable employees to take on jobs that are less stressful or demanding.

Providing partial-year employment opportunities so employees can spend the winter months in warmer climates, for instance, is another variation on phased retirement, Hoeck noted. Still another option on the upswing is inviting select retirees to return to work on a consulting or contingent basis, and offering training programs to redeploy retired workers who miss working and want to return to employment either full or part time, she said.

[SHRM members-only toolkit: Managing Flexible Work Arrangements]

Group Benefit Decisions

When putting phased retirement opportunities in place, employers should decide whether to maintain full health care and retirement plan benefits for those who are phasing into retirement—which is the approach most likely to keep older employees on board, benefit specialists say.

Alternatively, employers can reclassify program participants as part-time employees who are not entitled to group benefits, or they can provide a different benefit approach, such as offering subsidies for these workers to purchase health care on the individual market through the Affordable Care Act's (ACA's) marketplace exchanges. Employer subsidies can be made in pretax dollars through individual-coverage health reimbursement arrangements (ICHRAs), for instance. Smaller employers with fewer than 50 full-time or equivalent employees can provide similar subsidies through qualified small-employer HRAs (QSEHRAs). Those using a QSEHRA to buy an exchange policy may be eligible for a government tax credit or subsidy, which ICHRA participants are not eligible to receive.

If organizations choose not to offer full benefits for phased retirees, they should keep close watch on these employees' hours to ensure their part-time status is maintained, benefit advisors point out.

Many 401(k) plans permit in-service distributions after age 59 without penalties. Additionally, organizations with defined benefit pension plans can let near-retirees reduce their work hours and use partial distributions from the pension plans to supplement their reduced wages, as IRS rules allow pension distributions beginning at age 62 for those who are still employed, and the 2006 Pension Protection Act permits participants to collect partial plan benefits while phasing out of full-time employment.

For defined benefit plans, the salary component of the pension formula should be designed—or amended, if necessary—so that it is based, for instance, on plan participants' three consecutive highest-earning years, rather than their final three years of employment, pension advisors recommend.

Mentoring Younger Workers

Phased retirement programs also can be structured to encourage older workers to mentor younger colleagues who will take over their responsibilities.

"While granting pre-retirees the opportunity to continue earning income with the flexibility to retire on their own terms, employers can involve them in succession planning, mentoring and training, thereby facilitating more seamless transitions," Catherine Collinson, TCRS president and CEO, wrote in the third-quarter 2019 issue of Benefits Quarterly. "This is especially valuable in today's highly competitive, nearly full-employment labor market and will be for the foreseeable future as the critical mass of Baby Boomers retire."

PART 2: Targeted benefits for aging workers

| Related SHRM Articles: Phased Retirement Gets a Second Look, SHRM Online, June 2017 Taking Phased Retirement Options to the Next Level, SHRM Online, February 2017 Use Voluntary Benefits to Attract and Keep Part-Time Workers, SHRM Online, July 2017 Related SHRM Report: Preparing for an Aging Workforce: Strategies, Templates and Tools for HR Professionals, SHRM Research Guide, 2016 |

Related Articles

Learn how Marsh McLennan successfully boosts staff well-being with digital tools, improving productivity and work satisfaction for more than 20,000 employees.

The proliferation of artificial intelligence in the workplace, and the ensuing expected increase in productivity and efficiency, could help usher in the four-day workweek, some experts predict.

As artificial intelligence technology continues to develop, the demand for workers with the ability to work alongside and manage AI systems will increase. This means that workers who are not able to adapt and learn these new skills will be left behind in the job market.